One of the decisions taken at the European Council summit last week was an agreement that “To meet the objective of a climate-neutral EU by 2050 in line with the objectives of the Paris Agreement, the EU needs to increase its ambition for the coming decade and update its climate and energy policy framework. To that end, the European Council endorses a binding EU target of a net domestic reduction of at least 55% in greenhouse gas emissions by 2030 compared to 1990.”

The European Council thus endorsed the Commission’s proposal in its 2030 Climate Target Plan Communication for an EU-wide, economy-wide greenhouse gas emissions reduction target by 2030 compared to 1990 of at least 55% including emissions and removals. Note that this is a ‘net’ target including GHG removals through land use and forests, in contrast with the existing 40% target, which mainly concerns emissions only.

This means one cannot directly compare the current 2030 reduction target of 40% with the proposed reduction target of 55%, both relative to 1990. The 40% target refers mainly to emissions in the European Trading System (ETS) and Effort Sharing Regulation (ESR) sectors with only a very limited possibility to make use of Land use, Land use change and Forestry (LULUCF) credits as offsets (a maximum of 262 million tonnes CO2e for the EU27 over the 10-year 2021-2030 period). In addition, whether there are LULUCF credits or not is determined by policy-determined accounting rules and not by the inventory numbers. The net 55% target, however, will allow full offsetting of the LULUCF sink based on the LULUCF inventory numbers reported to the UNFCCC.

The proposed shift from a targeted reduction of 40% in gross emissions to a 55% reduction in net emissions has been criticised by environmental NGOs, partly on the grounds that the 55% figure is itself too low, but also because the shift from a gross to a net target is seen as a climate fudge and as creative accounting.

A coalition of environmental NGOs in a statement last September noted that “The Commission’s proposal to change the current 2030 target into a ‘net’ emissions target, including carbon sinks, is a serious mistake and – depending on the size of the net LULUCF sink – could mean real cuts in emissions of only 50.5-52.8%.” Greenpeace was quoted in this Guardian article as saying: “This accounting trick by the Commission would make any new target sound higher than it actually is.”

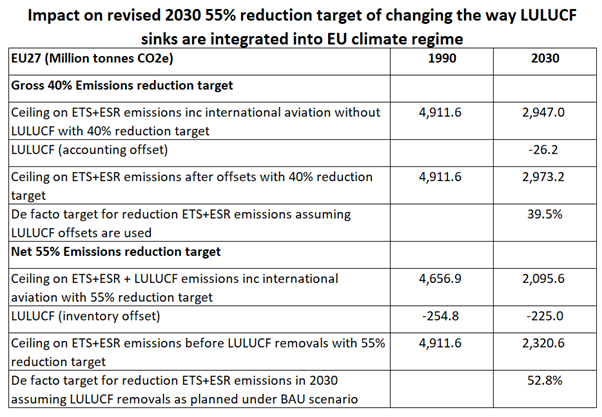

I drew the same conclusion in a table that I had included in this previous post where I mistakenly compared the proposed ‘net 55%’ reduction target to 1990 gross emissions. As the Guardian article makes clear, although it was not fully clear in the Commission’s presentation of its 2030 Climate Target Plan, the Commission will also change the 1990 base to a ‘net’ figure to be consistent with the format of the revised 2030 target. I therefore reproduce the corrected table below.

What we are interested in showing is what the change from gross to net accounting means for the level of ambition in reducing emissions from fossil fuels and agriculture (the ETS and ESR sectors combined). As the table below shows, changing to net accounting implies a lower level of ambition than if the 55% reduction was applied to gross ETS + ESR emissions as under the current 2030 framework (though not as low as were we to use 1990 gross emissions as the base as I had previously done).

The table shows the impact on the Commission’s 2030 climate ambition of allowing a larger LULUCF sink to offset emissions in the ETS and ESR sectors as they are currently defined (i.e. before adopting any of the proposed changes to the EU’s climate architecture put forward in the 2030 Climate Target Plan). Currently, flexibility is allowed only with the ESR sector, but the Impact Assessment opens the possibility for flexibility to the ETS as well. Two scenarios are shown. The first is the current 2030 target of a 40% reduction on 1990 levels with very limited integration of LULUCF credits.

The possibility to use some very limited offsets from the LULUCF sector against emissions in the ETS+ESR sectors reduces the necessary reduction in emissions in the ETS+ESR sectors very slightly, by 0.5%. According to the Impact Assessment for the 2018 ESR, the limited flexibility between the LULUCF and ESR sectors was a deliberate decision to avoid reducing the level of ambition in the ESR sector.

The second scenario is where the overall level of ambition is increased to a net 55% reduction in emissions by 2030, but the full LULUCF sink is included as an offset in both the base and target years. The projected LULUCF sink in 2030 is based on the Commission’s estimate of the size of the sink under the ‘no-debit’ rule in the Impact Assessment. This sink number would be higher in scenarios where additional sequestration in the LULUCF sector is incentivised. However, in assessing the stringency of the net 55% target the impact of additional effort in the LULUCF sector induced by the target should not be included.

The Impact Assessment also proposes a policy option where accounting rules would apply to make the contribution from the LULUCF sector more stringent, thus limiting the credits that could be transferred to other sectors but still permitting more flexibility than at present. However, the policy scenarios examined in the Impact Assessment all assume the full inclusion in the emission profile of removals in the LULUCF sector.

If an offset of the full LULUCF sink were allowed, it would reduce the reduction ambition in the ETS+ESR sectors to a reduction target of 53% rather than 55%. This implies that the level of ambition in the Commission’s Green Deal is less than what it first appears.

This post was written by Alan Matthews

Photo credit: Gerd Altmann on Pixabay used under a Creative Commons licence