In my previous post, I discussed the challenges of reducing non-CO2 greenhouse gas (GHG) emissions from agriculture and identified some of the strategies that are available or under development to allow farmers to reduce these emissions. But by how much would these strategies reduce projected emissions? What is the potential magnitude of the emissions reduction we should expect from agriculture in the coming decade? As in the previous post, I deliberately exclude a discussion of the potential to offset these emissions through land management and land use change although, as we will see, some insights into the potential to reduce emissions in the LULUCF sector will be covered in this post.

What I do in this post is to summarise the Commission’s quantification of the mitigation potential in agriculture up to 2030 in the context of the ‘Fit for 55’ package to be launched in June 2021. This is expected to propose significant changes in a raft of EU energy and climate laws to achieve the more ambitious at least net 55% emissions reduction target proposed for 2030. What contribution can we expect from reduced agricultural emissions towards the revised ‘at least a net 55% reduction’ 2030 target?

The post is an update to the excellent review by Allen and Maréchal ‘Agricultural GHG emissions: Determining the potential contribution to the Effort Sharing Regulation’ published by IEEP in 2017. Additional results are now available from the in-depth analysis of the ‘Clean Planet for All’ Communication in 2018, the impact assessment of the 2030 Climate Target Plan in 2020, as well as updated results from the Joint Research Centre ‘Economic assessment of GHG mitigation policy options for EU agriculture’ (EcAMPA) project. These are the results reported in this post.

Emissions trends under ‘business as usual’

First, a reminder of what the Commission expects to happen to agricultural emissions if no additional effort is made to reduce emissions, the baseline or ‘business as usual’ reference scenario. Based on the annual EEA inventories, agricultural emissions in the EU27 fell by 21% between 1990 and 2018, from 497MtCO2e to 394 MtCO2e (converting the non-CO2 gases to CO2e using AR4 weights).

The most plausible scenario to 2030 has been developed under the EcAMPA 4 project, the latest iteration of the EcAMPA initiative by researchers at the Joint Research Centre. This was published as a special chapter in the DG AGRI Market Outlook 2020-2030 publication last December. The EcAMPA project is based on the CAPRI model with mitigation technology options sourced from the GAINS model. Agricultural emissions are projected to fall to 388 MtCO2e by 2030 or by a further 1.6% compared to 2018. This reference scenario would bring the total reduction in agricultural emissions between 1990 and 2030 to 22%. This projection assumes a continuation of current CAP policies and no additional measures for GHG mitigation.

An alternative scenario using the GAINS model alone was published by a different group in the Commission in the impact assessment of its 2030 Climate Target Plan ‘Stepping up Europe’s 2030 Climate Ambition’ published in 2020. This analysis compares projected emissions in 2030 to emissions in 2005 and 2015. It projects a somewhat steeper decline in emissions by 2030 compared to EcAMPA 4 (a decline of 7% compared to 2015 levels). The 2020 impact assessment is conducted in terms of AR5 weights for non-CO2 gases, while the EcAMPA analysis uses AR4 weights. In the following analysis, I also make use of its figures for mitigation potential.

Mitigation potential from further measures targeting non-CO2 gases

There are various measures of mitigation potential, including technical, economic and market potentials. The technical mitigation potential measures the maximum mitigation possible with full implementation of all available mitigation measures and ignoring barriers to adoption. Economic potential includes only those measures that are cost-effective at a given carbon price. The market potential considers social, cultural, farm-level and political constraints to adoption that restrict the use of mitigation measures, often linked to concerns about adverse effects on farm income.

The Commission’s 2018 in-depth analysis of the ‘Clean Planet for All’ Communication took 2050 as the target date rather than 2030 which is the main focus of this post. However, for completeness I include it here. In the baseline, the impact assessment projected agricultural emissions to remain broadly stable until 2050 at 2010 levels in the absence of further mitigation incentives or changes in amount and type of agriculture goods produced. At a carbon price of €200/tonne CO2e, it projected an economic mitigation potential of around 130 MtCO2e in 2050. With baseline agricultural emissions remaining at around 400 MtCO2e in 2050, this represents a mitigation potential of 33% compared to the baseline.

We observed in the previous post that the Commission’s modelling for the impact assessment of the 2030 Climate Target Plan calculated that the potential for mitigating agricultural non-CO2 emissions ranged from 12.3 MtCO2e to 30.6 MtCO2e at CO2e prices varying between €0 and €55 per tonne CO2e. These reductions can be compared to projected baseline 2030 emissions in that Commission report of 375 MtCO2e (measured using AR5 weights to convert non-CO2 gases to CO2 equivalents) (figures taken from Tables 42 and 44 in the impact assessment part 2/2). They correspond to reductions of between 3% and 8% of baseline emissions in 2030.

Further reductions are expected arising from implementation of targets stemming from the Biodiversity and Farm to Fork Strategies in Member States’ CAP Strategic Plans. In an as yet undisclosed report (it is apparently still undergoing review, but the results are reported on page 90 of the impact assessment 2/2), the Joint Research Centre modelled the impact of the Commission’s proposals and projected a 17.4% reduction of non-CO2 GHG emissions in the agricultural sector by 2030, going up to 19.0% with the additional budget made available under the “Next Generation EU”. One assumes that these figures have been derived from the CAPRI model in the EcAMPA project but as the study has not yet been published, it is not clear how this potential was measured – what mitigation options were considered, whether it assumes full implementation of the quantitative targets included in these Strategies regardless of cost, whether each Member State is assumed to meet the targets separately, or whether the Strategies were implemented in some other way.

Another set of results reported in the DG AGRI Market Outlook publication is based on a previous iteration of the EcAMPA project, the EcAMPA 3 study by the Joint Research Centre (Pérez Domínguez et al, 2020). It reports that adoption of mitigation practices and technologies incentivised by pricing non-CO2 emissions has the potential to lead to a reduction of between 15 and 35 MtCO2e in agricultural emissions where the CO2e price varies between €20 and €100 per tonne CO2e. These figures are similar to those estimated in the 2030 Climate Target Plan impact assessment, though allowance must be made for differences in the metrics used.

The EcAMPA 3 iteration incorporated a carbon cycle model into the underlying CAPRI model used for simulations. This allows the model to report changes in soil carbon stocks resulting from changes in land management and land use to be calculated as well as reductions in non-CO2 gases. DG AGRI reports that the EcAMPA 3 iteration estimated that, at the same carbon prices (between €20 and €100/t CO2e), there would be a further reduction in LULUCF emissions of between 37 and 45 MtCO2, making a total mitigation potential of up to 80MtCO2e.

It is important to underline that this LULUCF mitigation arises solely as a by-product of targeting non-CO2 gases only in the model. The CO2 savings in the LULUCF sector are a secondary effect resulting from imposing a carbon price on non-CO2 emissions only. They should not be taken to represent the potential LULUCF abatement if, for example, a carbon farming scheme were introduced that in addition put a price on CO2.

These reductions refer to the direct impacts of implementing these practices. Because these practices are costly, they will induce further changes in production levels and production mix as farmers reassess their production decisions in the light of the new cost structures. The DG AGRI Market Outlook observes that, when changes in production intensity and production mix following the imposition of a carbon price on non-CO2 emissions are included, these emissions savings are amplified, by a further 40% at the lower carbon price (€20/tonne) and by a whopping 180% at a carbon price of €100/tonne. At the higher carbon price, the mitigation potential in agriculture including LULUCF reductions could be as high as 224 MtCO2e (i.e., 80 Mt CO2e * 2.8).

To understand where these figures come from, it is helpful to take a closer look at the EcAMPA 3 study.

A closer look at the EcAMPA 3 study

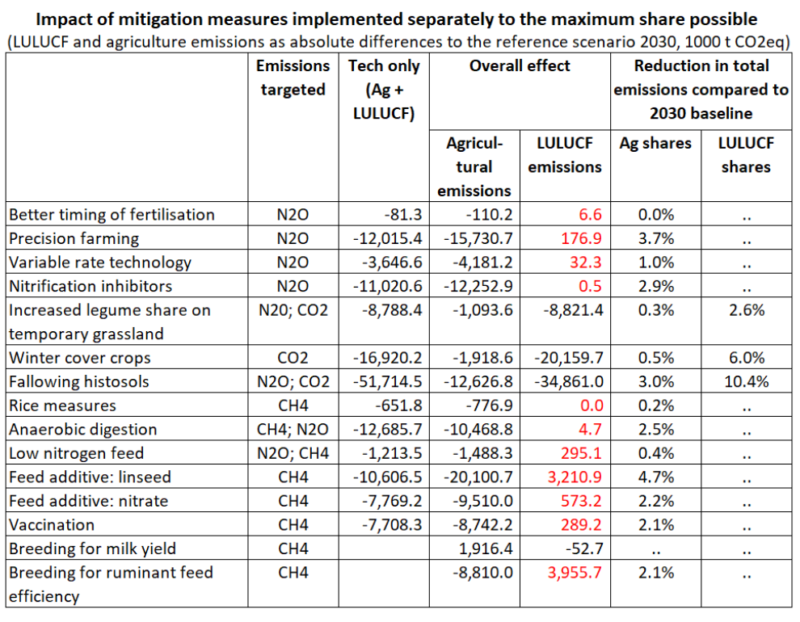

What are the mitigation practices that would give rise to these abatement potentials? The following table shows the technologies included in the EcAMPA 3 study and their mitigation potential under various assumptions. All technologies focus on non-CO2 gases but in some cases there can also be an indirect effect on CO2 emissions. Three of the measures shown in the table – increased share of legumes in temporary grasslands, winter cover crops, and the fallowing of organic and peat soils (histosols) – are included because they can help to reduce N2O emissions, but if implemented their contribution to reducing CO2 emissions would be much more important.

The mitigation potential shown in this table is the (theoretical) maximum technical mitigation potential for each mitigation option assuming that it is applied to the maximum extent possible. The figures are calculated by turning on each mitigation technology one at a time, while freezing the uptake of the other technologies to their baseline levels. Results for two scenarios are shown for each technology (except for the breeding technologies where this does not make sense).

The first scenario is the ‘tech only’ option. This estimates the direct impact of the applied technology, assuming no response by farmers in terms of production levels or production mix. We can think of this as a scenario where the introduction of the technology is fully subsidised so there is no change in farmers’ costs. This direct impact includes reductions in both non-CO2 emissions as well as CO2 emissions from land. Both impacts are added together and shown as a combined total in the table.

The second scenario is the ‘overall effect’. This scenario assumes there is a cost associated with adopting the technologies, so their forced adoption leads to adjustments in the optimal land use allocation and livestock production. These adjustments in the production intensity and production mix are due to the profit maximization framework of CAPRI. This overall effect is separated into the reduction of agricultural emissions and the change in LULUCF net emissions/removals in the table.

For each technological mitigation option the net effect on the aggregated LULUCF and agriculture emissions is a reduction in total emissions. In general, the positive mitigation effect (‘tech only’) on the ‘targeted’ emissions type is augmented once the land use allocation is adjusted to the application of the mitigation technology (though not in the case of fallowing histosols or anaerobic digestion). The ‘forced’ adoption of mitigation options reduces profitability, and this income loss is minimised by shifting away from the affected activities.

Relative costs of mitigation technologies in EcAMPA 3

The previous table does not tell us anything about the relative costs of pursuing mitigation through the different technological options. Costs in the EcAMPA project are of two kinds. The first type are the accounting costs (amortised investment costs plus annual implementation costs) of the mitigation option. The second kind refer to ‘adoption costs’. Even where a more profitable technology arrives, not all farmers adopt it immediately. CAPRI considers this is due to costs that are known to farmers but not included in accounting costs that increase more than proportionally as use of the technology expands.

Examples might be labour or machinery bottlenecks, risk premiums or rotation constraints. For this reason, the unit cost of adoption by the last farmer is assumed to be higher than for early adopters. These non-linear adoption costs have a further modelling advantage that they smooth adjustments to changes in technology and avoid sudden and large switches in production that would occur under a simple linear programming model.

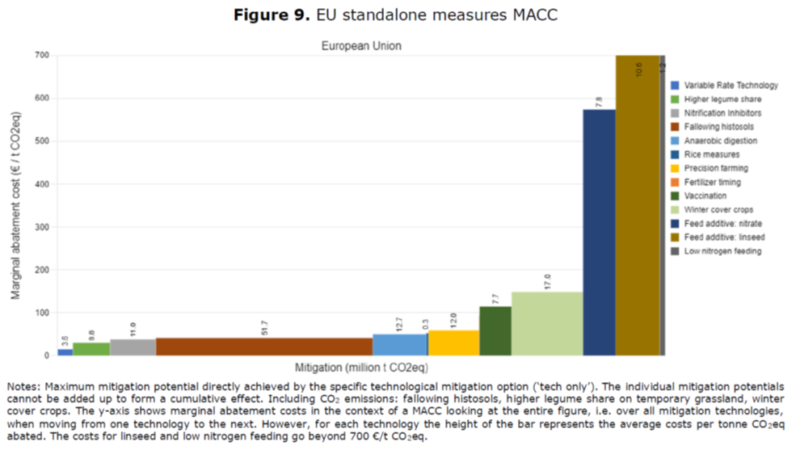

The next chart shows the average unit costs of each mitigation option (averaged over all adopters) on a stand-alone basis, that is, when each option is implemented on its own to the maximum technical extent possible. The mitigation achieved for each option (shown by the horizontal width of each option) does not take into account induced changes in production, so it corresponds to the column heading ‘tech only’ in the previous table.

The attractive measures are those with high mitigation potential and low abatement cost. They include nitrification inhibitors, fallowing of histosols, anaerobic digestion, precision farming, variable rate technology and higher legume share on temporary grassland. On the other hand, measures such as vaccination against methanogenic bacteria in the rumen, winter cover crops, and the two feed additives nitrate and linseed can deliver high mitigation but at high cost. For the two feed additives, EcAMPA estimates the average cost would be over €700/t CO2e abated.

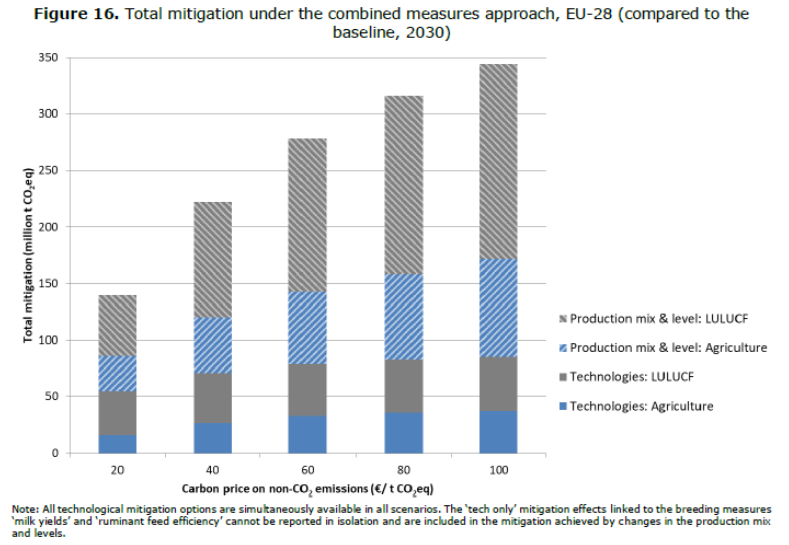

An alternative way to present the mitigation abatement cost curve is through a combined approach. All technological mitigation options are assumed to be available at the same time and can be adopted cumulatively by farmers. Adoption rates and mitigation potential will depend on the relative costs of each option (which will vary depending on the existing level of uptake) and the carbon price applied in different scenarios. This carbon price is only applied to non-CO2 emissions. The following chart shows the projected mitigation potential and the practices that contribute to this potential at different carbon prices between €20 and €100 per tonne CO2e. This mitigation potential includes both the direct abatement due to the use of the mitigation technologies and the associated changes in production intensity and production mix.

The solid rectangles at the bottom of each column show the direct contributions of the technological options to the total mitigation achieved under the combined measures approach at aggregated EU-28 level. The abatement potential for the technologies assessed in the EcAMPA 3 project amounts at the highest carbon price to 85 MtCO2e including emissions reductions in the LULUCF sector. This corresponds to the 80 MtCOe reported in the DG AGRI chapter, the difference most likely arising because the results reported in Pérez Domínguez et al, 2020 refer to the EU28, while the DG AGRI results refer to the EU27 following Brexit.

By far the highest mitigation is achieved by fallowing histosols at all carbon price levels. In fact, it realises about 75% of its maximum potential already at a carbon price of €20/t and further increase is limited. This is followed by anaerobic digestion, higher legume share on temporary grassland, winter cover crops and nitrification inhibitors as well as the feed additives and vaccination against methanogenic bacteria in the rumen. Some of these measures were classified as high-cost in the stand-alone approach. Their appearance in the combined measures approach indicates that they can be cost-effective at least for some farmers in some regions.

The chart makes clear, however, that most of the abatement potential arises from changes in production levels and production mix rather than from direct application of the chosen mitigation technologies (these are the two stippled rectangles at the top of each column). At the lower carbon price 61% of the abatement potential shown in the previous chart comes from production changes. This share increases as the carbon price increases, and accounts for 75% of the total abatement when the carbon price reaches €100 per tonne. The effects of the breeding measures related to milk yields and ruminant feed efficiency are included as part of the production level and mix changes. At the highest carbon price, the total mitigation potential reaches almost 350 MtCO2e. Somewhat surprisingly, this figure is reported in the DG AGRI Market Outlook chapter as 224 MtCO2e which is a considerable drop even allowing for the impact of the departure of the UK on these figures.

Another striking finding is that, on average, about 65% of the total mitigation in the scenarios relates to avoidance of CO2 emissions and carbon sequestration (reported in the LULUCF sector). This LULUCF contribution arises both from the direct effects of the technology as well as from subsequent changes in production levels and production mix. However, it is still only a secondary effect as the carbon price targets only non-CO2 emissions from EU agriculture.

The DG AGRI chapter also reports changes in soil organic carbon (SOC) arising from the baseline projections of agricultural output to 2030 in EcAMPA 4. SOC is increased as a result of increasing organic inputs to the soil and/or decreasing their loss or slowing down the mineralisation process. Organic inputs consist mainly of crop residues (including root inputs), manure from grazing animals and manure spread over the field. The study estimates this increase to be around 10 MtCO2 annually to 2030.

The impact of the three mitigation options with significant impacts on CO2 emissions included in the first table should be added to this. In the EcAMPA 3 publication, summing the LULUCF reduction in removals in the ‘overall effect’ column in the first table amounts to 64 MtCO2. The figure quoted in the DG AGRI report (for a smaller EU27) is 75 MtCO2. These estimates assume each of these measures are implemented on a stand-alone basis, assume no interactions between them, and include the indirect effects on production.

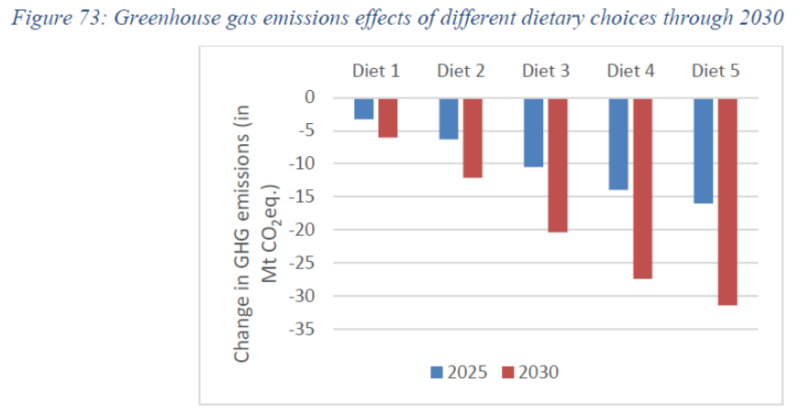

The impact of diet changes

Diet changes are expected to play an important role in reducing EU agricultural emissions (see previous post). However, dietary changes have not been explicitly modelled in the studies under review. The Commission 2030 Climate Target Plan impact assessment refers to a sensitivity analysis undertaken as part of the in-depth analysis accompanying its 2018 ‘Clean Planet for All’ Communication to understand the possible implications of differing trends in consumer preferences by the EU population on greenhouse gas emissions in the next decades.

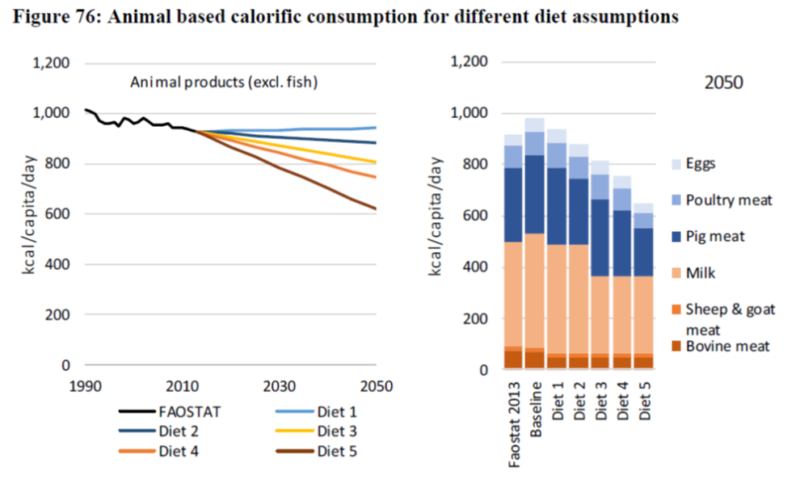

Five diet scenarios were analysed in addition to the baseline which is based on the same assumptions as the EU Reference Scenario 2016. Diet 5 was seen as consistent with reaching in 2070 levels of meat consumption in line with recommended diets in several studies. Each scenario also included a reduction by half in the generation of food waste in all EU Member States. The following chart shows the total calories contributed by animal source foods in the different diets (on the left) and the contribution of the different foods to the overall total in 2050 (on the right).

The analysis assumes that the decrease in EU animal products consumption is entirely reflected in EU production levels and no increase in exports of animal products to the rest of the world takes place. Under that rather heroic assumption, the 2020 impact assessment concluded that the potential emissions reduction from dietary change by 2030 could be of a similar order of magnitude to the technical reduction potentials in the agricultural sector.

Conclusions

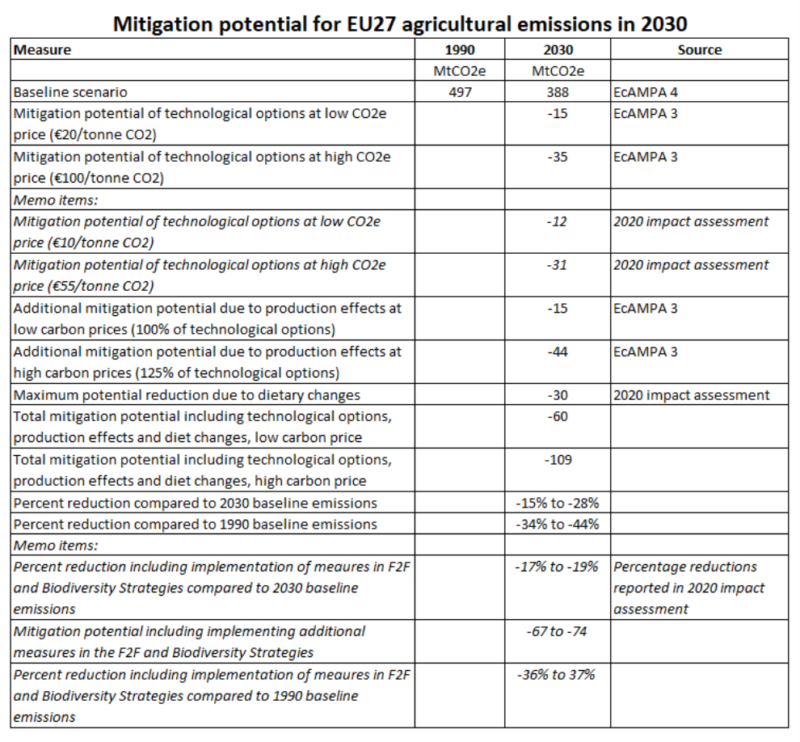

In the spirit of Allen and Maréchal’s review of estimates of the mitigation potential in EU agriculture which covered studies up to 2017, this post extends their review to take account of more recent studies by the Commission. The following table provides an overall summary of the findings. The table mainly uses estimates from the JRC’s EcAMPA 3 project, supplemented by information from the Commission’s impact assessment for the revised 2030 emission reduction target.

It is a complex table but the following main points can be highlighted. It concentrates on the abatement potential for non-CO2 emissions from agriculture, although we saw that the secondary emissions reductions in the LULUCF sector will likely be more important. The emissions reductions from the technological options included in the EcAMPA 3 project are first reported, both for low (€20/tonne) and high (€100/tonne) CO2e prices. These are compared to the corresponding abatement potentials reported in the Commission’s impact assessment for the 2030 Climate Target Plan. Although both studies use different carbon price scenarios, and use different weights to aggregate non-CO2 gases to CO2 equivalents, there is broad agreement in their findings.

The next part of the table adds the abatement potential from production changes that would occur when levying a carbon price on non-CO2 emissions, again for the low and high carbon price scenarios. It also shows the upper end estimate for potential reductions due to dietary changes up to 2030. The total mitigation potential is estimated by adding these three elements together, assuming no interactions between them. This certainly overestimates the maximum potential mitigation as some of the production changes induced by the dietary changes may overlap with the changes induced by implementing the technological options.

As a benchmark, the estimated reduction potential from implementing the Farm to Fork and Biodiversity Strategies is also shown. We stress again that these are results from an unpublished study so the measures included in that simulation are not known. For example, whether it includes some demand-side changes from the food waste reduction target in the F2F Strategy, what carbon price is assumed, or whether it includes the production impacts of the technological options selected, is not known.

Despite these caveats, the conclusion from the table is that there is potential for mitigation in the agricultural sector, but this depends on how willing we are to see production fall. Without any production impacts, the adoption of technological options alone would reduce agricultural emissions by between 4-9% below the 2030 baseline depending on the carbon price. Allowing for production impacts including from the impact of dietary changes, the modelling studies suggest that a reduction in agricultural emissions even at a low carbon price of between 15-17% below the baseline trend would be a realistic target by 2030. At higher carbon prices (implying greater policy efforts and greater production impacts) this could increase up to 28%.

Still, reducing agricultural emissions is more challenging than in other sectors. The low-end estimate for agricultural emissions reduction in 2030 even including production impacts compared to 1990 is 34% when the EU economy as a whole is aiming for a net reduction in emissions of 55% (implying a gross reduction of around 53%). However, if a greater impact on production is deemed acceptable, the percentage decrease in agricultural emissions could be even higher. Further secondary emissions reductions take place in the land sector but these would be reported separately under the LULUCF heading in the inventories.

These estimates depend on heroic assumptions about accounting costs, their rate of change over time as technology advances, and adoption rates. Previous literature has shown that the range for these accounting costs is very wide. There may also be wide differences in the abatement expected from a particular practice, not least because agricultural emissions are due to biological processes that are influenced by soil type, temperature, precipitation, and management practices. Given these uncertainties, any estimate of the mitigation potential in agriculture should be reviewed with a critical eye.

One example can be given from the studies reviewed in this post. Both the Commission impact assessment and the JRC EcAMPA studies rely on the GAINS database for the costs and mitigation potential of different mitigation technologies. While the EcAMPA 3 study sees great potential in the fallowing of histosols (75% of the technical potential would already be exploited at a carbon price of €20/tonne CO2e), this technology would not figure in the Commission’s mitigation cost curve until the carbon price is well over €100/tonne CO2e (see Figure 74 in the Commission’s 2018 in-depth analysis). Part of the explanation is that the EcAMPA 3 study also counted the (considerable) CO2 mitigation in the land sector, even when the technology is incentivised by a carbon price on non-CO2 gases.

The mitigation potentials shown in the previous table reflect the estimated cost-effective potential at different carbon prices. Carbon prices are not currently an instrument used to abate agricultural emissions and are used to stimulate a response in the different models. They are an indication of the relative stringency of the policy measures that might be used to incentivise mitigation reductions of this magnitude.

One might also surmise that the instruments used might influence the rate of adoption of the different measures. Both the EcAMPA project and the GAINS model try to model adoption rates so some account is already taken of resistance to implementing the mitigation options. My instinct is that these adoption costs underplay the difficulty of organising mitigation actions on the ground given the millions of individual actors who are expected to play a role.

The big unknown from the published studies to date is what the production impacts included in these figures mean for production levels and farm incomes in the EU. The EcAMPA 3 study was intended primarily to show ‘proof of concept’ and to demonstrate the implementation of the carbon cycle model in CAPRI. It did not give details of the production impacts or impacts on farm income of setting carbon prices at these levels. Nor did it indicate the extent to which these emissions might be shifted off-shore if domestic EU production is replaced by increased production elsewhere.

This information may be included in the yet-to-be-disclosed study of the impact of implementing the Farm to Fork and Biodiversity Strategies referred to in the Commission’s impact assessment of the 2030 Climate Target Plan or in the as yet unpublished EcAMPA 4 study if this is different. Until now, it has been taboo to discuss policy interventions that have a significant negative impact on agricultural production in the EU. This taboo was broken with the publication of the F2F Strategy where several of the interventions highlighted will result in lower EU production. Knowing the production and farm income impacts will help to better evaluate the political feasibility of reaching the 2030 mitigation potential projected in these studies.

This post was written by Alan Matthews.

Update 7 April 2021: The method used to calculate the additional reduction due to production impacts in the summary table was changed. The conclusions were redrafted to emphasise more the contribution of production impacts.

Photo credit: Pxhere, used under a Creative Commons licence

Does the EcAMPA3 study take into account that certain measures might not be as easily combined, or does it look at the technical reduction potential of each measure separate?

@Laura, thanks for question, it actually does both. So the graph labelled ‘Figure 9’ in the post is the stand-alone version where the technical potential of each measure is examined separately, and the graph labelled ‘Figure 16’ is based on a combined approach which explicitly takes account of the fact that certain measures might not be easily combined, as you suggest.

I am very impressed with the mission of the company https://slopehelper.com/ “No more hands in agriculture”. I really think this is where agriculture should aim

This is hugely helpful Alan for understanding the interplay between the moving parts. It’s interesting to see that the modelled diets include a reduction in pig and poultry consumption (not just ruminant products) which presumably has a knock-on effect on cereal production/soya imports and therefore land use decisions.. the F2F impact study will be helpful if the taboo on reducing production is really broken, and might even help guide the new administration here in Scotland on actually helping agriculture get with the programme on reducing emissions