My previous post discussed the rationale for the Commission’s revised MFF proposal put forward on 27 May 2020 which includes a proposal for a European Recovery Instrument (ERI) to finance front-loaded expenditure in the next MFF plus a slightly revised ‘standard’ MFF (which the Commission refers to as a ‘reinforced’ MFF). In broad terms, the reinforced MFF allows for commitment appropriations amounting to €1,100 billion over the 2021-2027 period, while the ERI would help to finance a further €750 billion of spending in the 2021-2024 period, in constant 2018 prices. Together, they add up to a total proposed spending of €1,850 billion over the MFF period.

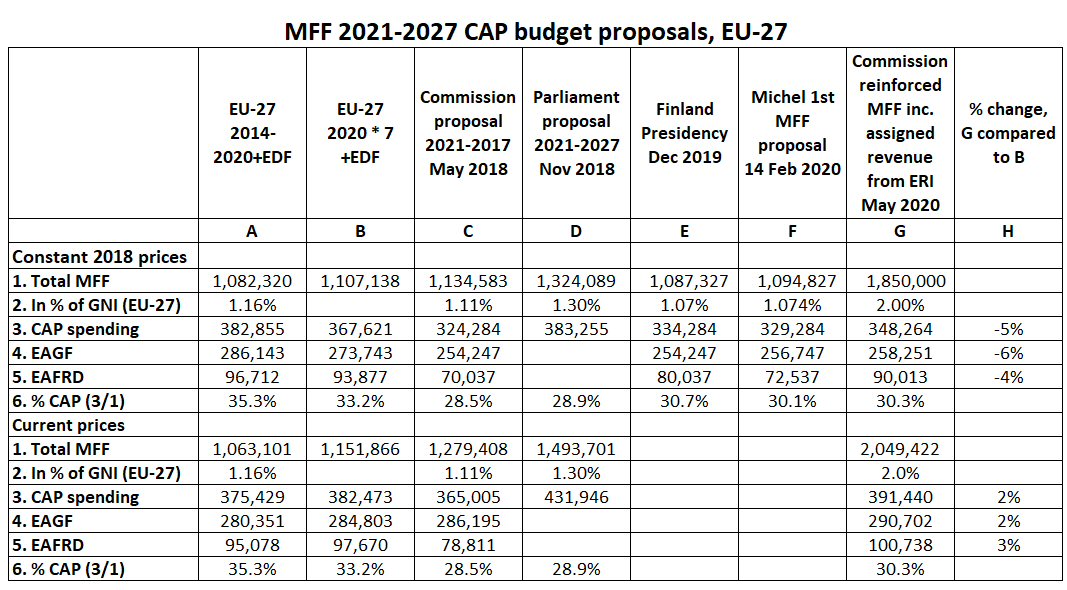

The following table tracks the debate on the overall size of the MFF since the Commission’s initial proposal in May 2018. It also describes the allocation for the CAP budget in the various proposals. The farm unions and their supporters have paid particular attention to comparing the latest Commission proposal with commitment appropriations under the current MFF. There is no unique or right way to make this comparison. In this post, I examine the issues involved.

Note. The Commission Questions and Answers on the EU budget: the Common Agricultural Policy and Common Fisheries Policy reports that the latest Commission proposal is a 2% increase in constant 2018 prices over the 2014-2020 baseline, the same as in current price terms. This does not seem plausible and the reason for the discrepancy with the figure I estimate in this table is not clear.

As a first comment, it is worth highlighting that, excluding the ERI, the reinforced MFF total in constant 2018 prices of €1,100 billion is still well below the Commission’s original MFF proposal in May 2018. Indeed, it is only a very small increase over the first MFF negotiating box presented by European Council President Charles Michel to the European Council on 14 February 2020. This received such harsh criticism from Member States that Michel circulated amendments to this proposal in the course of the meeting itself, which reduced the overall MFF volume further to €1.069 billion. As this was not a formal proposal (it consisted of two pages of loosely-drafted amendments) I have not included it in the table above. The new Commission proposal is a very minor ‘reinforcement’ of the MFF totals compared to the February 2020 negotiating box.

The table highlights two of the issues in making comparisons between the CAP budget in the next MFF and the current MFF. The first is the appropriate baseline to use. One alternative is to take the total commitment appropriations in the 2014-2020 MFF as the baseline. This is what the European Parliament does in its Resolution adopting its interim position on the MFF in November 2018. The other alternative is to take commitment appropriations in the final year of the current MFF and multiply it by seven to get a ‘baseline’ allocation to serve as the comparator. This is the Commission’s preferred approach as set out in this Questions and Answers on CAP spending in the EU Budget. In both cases, pre-defined allocations to the UK have been deducted to generate an EU27 baseline.

The Commission’s preferred approach provides a lower baseline in constant 2018 prices but a higher baseline in current prices compared to the Parliament’s use of committed resources over the whole MFF period.

A second issue is whether the comparison is made in constant (2018) or current prices. Again, there is no uniquely correct approach. The MFF Regulation sets out commitment appropriations each year in constant prices. It also specifies that these are converted to current prices using a fixed 2% annual deflator. These current price amounts are what are shown in the Annexes in the CAP Strategic Plans Regulation which set out the annual pre-allocated ceilings for direct payment and rural development spending for each Member State. The table above shows that, using the Commission’s baseline for the 2014-2020 MFF as the comparator, its proposal implies a 5% fall in constant prices, but a 2% increase in current prices.

Commissioner Wojciechowski was particularly at pains in his press conference following the publication of the Commission’s MFF proposal to highlight this increase in current prices not only relative to the current MFF but even more so with respect to the Commission’s original MFF proposal. In current prices there is now €26.5 billion more for the CAP compared to what the Commission proposed two years ago.

Real, constant and nominal prices: a discursion

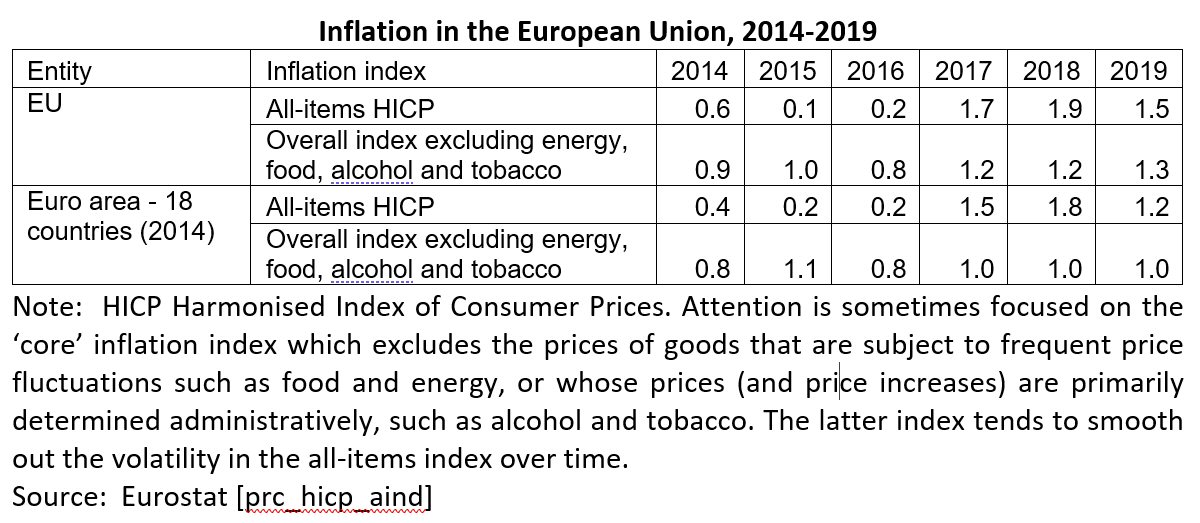

The farm unions have criticised the Commission proposal because they claim it fails to maintain the value of payments in line with inflation. They make this criticism pointing to the reduction in the CAP budget in constant 2018 prices. But there is a subtlety in the constant price figures that is often ignored. These figures are often presented as being in ‘real’ terms. A cut in real terms implies that the money received by farmers will purchase fewer real goods and services in the future. But constant price figures will only represent ‘real’ amounts if the actual rate of increase in the prices of real goods and services (the rate of inflation) is exactly equal to the 2% deflator set out in the MFF Regulation.

Each year, the Commission updates the MFF ceilings by 2% to convert to current prices. However, if the rate of inflation in that year is 3%, then the real value of a fixed MFF amount in constant prices would actually fall, by 1%. Conversely, if the Commission increases the ceilings by 2% but the actual rate of inflation is only 1%, then the real value of payments to farmers increases, in this case also by 1%.

For the eurozone, the European Central Bank has a price stability mandate that it interprets as maintaining inflation rates below, but close to, 2% over the medium term. But the real problem in recent years has been that inflation has been too low, and this seems likely to continue in the immediate future. The ECB flash estimate for inflation in the eurozone in May 2020 is -0.1%.

What this means for future agricultural spending is that a budget that is held constant in constant prices could imply an increase in the real value of that spending if future inflation is less than 2%. Put another way, an agricultural budget that is cut in constant price terms could still maintain the real value of farm payments depending on the future rate of inflation.

Of course, if we want to compare the ‘real’ value of the agricultural budget included in the Commission’s latest MFF proposal with the ‘real’ value of the agricultural budget included in the current 2014-2020 MFF, the current price MFF figures should also be deflated by the actual rate of inflation. Here, Eurostat figures show that actual inflation particularly in 2014-2016 was well below the MFF 2% deflator, implying a 1% annual gain in the real value of farm payments over this period.

If this pattern continues into the next MFF, then the ‘real’ value of farm payments will be 7% higher at the end of the MFF period relative to the trend shown in constant prices. This would effectively more than wipe out the apparent ‘cut’ in farm payments in constant prices, and would maintain the value of CAP payments in ‘real’ terms. Yet this adjustment is never acknowledged in the public debate.

There are other subtleties in the CAP budget that are also often forgotten. Massot and Negre (2018) point out that EAGF payments can often by higher than the appropriated amounts because of the existence of assigned revenue. ‘Assigned revenue’ includes the recovery of funds from the CAP as well as the fresh carry-overs of those recoveries. They estimate that assigned revenue to Pillar 1 could amount to €1,160 million for the 2021/2027 period in current prices (which would be added to the EAGFs sub-ceiling of €290.7 billion in current prices under the last Commission proposal).

Furthermore, the MFF includes an entry for ‘Margins’ under each of its main Headings to allow for contingencies. In the Commission’s May 2018 MFF proposal, the total margin for Heading 3 ‘Natural Resources and the Environment’ was €814 million (€918 million in current prices) over the whole MFF period. In principle, this could be budgetised for CAP expenditure if emergency needs arise. In the latest Commission proposal, this margin has been increased to €1.5 billion in constant prices (€1.7 billion in current prices).

Finally, the Commission has maintained the EU co-financing rates for rural development in the revised proposal at the ones proposed in May 2018: 70% for less developed regions, POSEI and Aegean islands; 43% for other regions; 65% for agri-environmental support; 80% for certain rural development support (e.g. LEADER); 100% for amounts transferred from direct payments. Readers will recall that this implied a 10 percentage point increase in national contributions to EAFRD spending. When this is factored in, it represents a further increase in the total transfers to farmers from both EU and national sources.

The conclusion from this analysis if that, if inflation remains subdued in the next MFF period (implying an inflation rate of around 1% rather than 2% per annum), then the Commission proposal would actually maintain the real value of the CAP budget as the farm unions request. While predicting macroeconomic indicators so far into the future is always risky, this does not seem to be an unreasonable assumption at this point in time.

Pillar 1 under the hood

The overall budget figures are one thing; equally important is the use that is made of them. The Pillar 1 (EAGF) budget is used for pre-allocated amounts to Member States (direct payment envelopes and sectoral interventions) and for market-related expenditure. The criticism in the current MFF has been that the provision for crisis market-related expenditure has not been sufficient.

Pillar 1 has received an increase of €4.0 billion in constant 2018 prices (€4.5 billion in current prices) compared to the Commission’s May 2018 MFF proposal. No change is proposed in the ceilings for direct payments and sectoral interventions. Thus, the Commission’s figures for the direct payment ceilings by Member State in its 2018 proposal remain valid for the CAP transitional Regulation currently in trilogue between the Council and Parliament. All of the proposed increase will be reserved for market-related expenditure. According to the Commission’s budget communication, this money is intended for “Strengthening the resilience of the agri-food and fisheries sectors and providing the necessary scope for crisis management”.

Apart from a general sense that more headroom should be included in the CAP budget to address crisis management, it is likely that this additional money covers the €1 billion safety net instrument promised by the former Agriculture Commissioner Phil Hogan to address potential market disruption if the EU-Mercosur Free Trade Agreement enters into force. It is also highly likely that the Commission wants to prepare for possible market disruption at the beginning of next year if the UK-EU free trade negotiations end in a ‘hard Brexit’.

Pillar 2 under the hood

The increase in Pillar 2 commitments comes from two separate pots: on the one hand, there is an increase of €5 billion in constant 2018 prices (€5.6 billion in current prices) in the reinforced MFF; on the other hand, there is a €15 billion top-up from the ERI (€16.5 billion in current prices) which will contribute as assigned revenue to Pillar 2 expenditure.

The different sources for this additional financing make a difference to how the money can be used. The increase in MFF appropriations will be available throughout the MFF period for standard rural development interventions decided under the national CAP Strategic Plans. This money will also be subject to various limits set out in Article 86 of the Strategic Plans Regulation. For example, at least 5% must be reserved for LEADER, and at least 30% must be reserved for interventions addressing the three environment and climate-related specific objectives set out for the coming CAP.

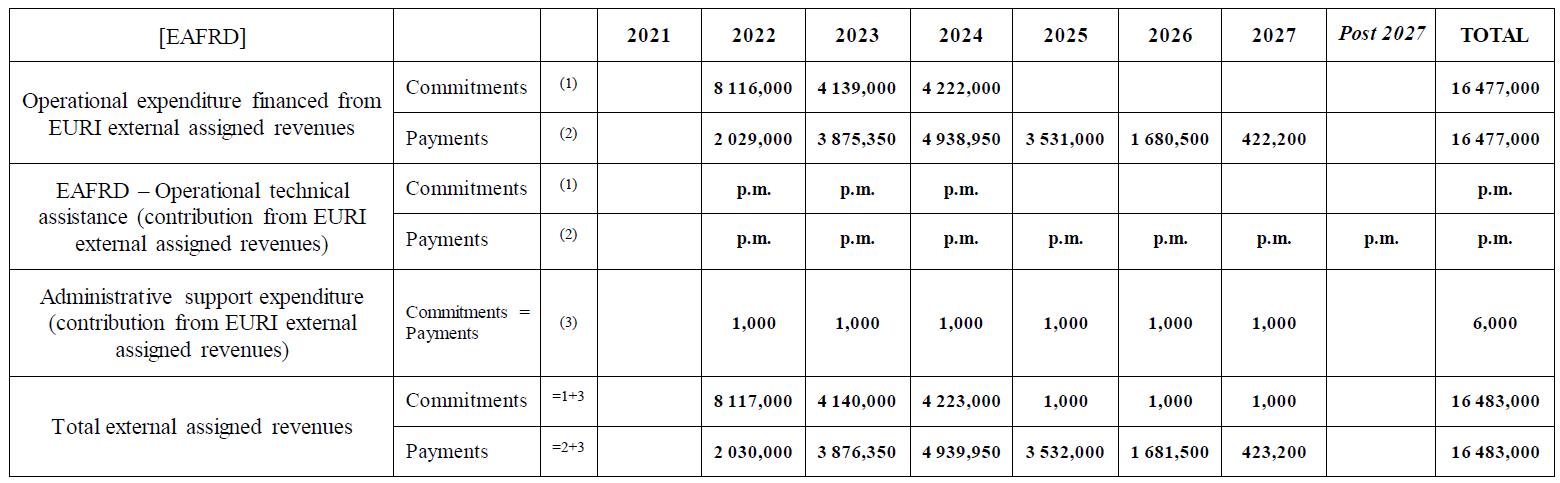

For the ERI assigned revenue, this money must be committed within the three years 2022-2024, although payments can continue to be made in later years (the indicative sequencing of commitment and payment appropriations for the EAFRD funding is shown in the following table).

It is intended that the allocation of these additional resources by Member State will follow the distribution key set down in the original SP Regulation.

There is some ambiguity around the kinds of interventions for which this ERI money can be used. Although the Agriculture Commissioner has indicated that the additional EAFRD financing should be used to support the green transition as set out in the Commission’s Farm to Fork and Biodiversity Strategies, the legislation puts more emphasis on responding to COVID-19. Is the ERI funding intended mainly to address the fall-out from the COVID-19 measures, or is it intended to support the farming sector in the transition to the European Green Deal?

According to the Commission’s proposal for the European Recovery Instrument [Next Generation EU], Recital (6) states: “As the Instrument is an exceptional response to these temporary but extreme circumstances, the support under the Instrument should only be made available in order to address the consequences of the COVID-19 pandemic or the immediate funding needs to avoid a re-emergence of the COVID-19 pandemic.” In Recital (7), it notes specifically that the Instrument should “support rural areas in addressing the impact of the Covid-19 pandemic”.

Article 2 of the ERI Regulation ‘Scope of the Instrument’ gives as one objective to “(i) support measures to address the impact of the COVID-19 pandemic on agriculture and rural development”. This seems a rather narrow interpretation of what the additional €15 billion might be used for.

In the Commission’s Omnibus Regulation legislative proposal that, inter alia, amends the CAP Strategic Plan Regulation to provide for external financing through the ERI, a new recital 71(a) confirms that the intention is that “recovery and resilience measures under the European Agricultural Fund for Rural Development should be carried out to address the unprecedented impact of the COVID-19 crisis”. Note there is no mention in these texts of the green and digital transitions.

The explanatory material accompanying the Omnibus legislative proposal does suggest a potentially broader scope for the use of these funds: “The instrument should also reinforce support, through the European Agricultural Fund for Rural Development (EAFRD), making available for Member States exceptional additional resources to provide assistance to the farming and food sectors that have been hardly hit, for fostering crisis repair in the context of the COVID-19 outbreak and preparing the recovery of the economy”

However, it seems that we have not yet seen the full package from the Commission.

In the proposed amendment Article 84a to the CAP Strategic Plans Regulation there are two noteworthy provisions. One is paragraph 4 which states that Article 86 of the SP Regulation (setting out minimum and maximum amounts of financial allocations) does not apply to the additional ERI €15 billion. As this is the Article that requires at least 30% of the EAFRD funding to be used for environment and climate-related interventions, it is no surprise that environmental NGOs on social media have expressed alarm about this apparent backsliding.

On the other hand, it appears (under paragraph 6 of this new Article 84a) that “The additional resources [under the ERI] shall be used under a new specific objective complementing the specific objectives set out in Article 6 to support operations preparing the recovery of the economy”. In other words, it appears that the Commission plans to introduce a new, tenth, specific objective but no further details are given. It is strange that an amendment to set out this new specific objective was not already included in this Omnibus legislative proposal which is the obvious place for it. It may be that in the rush to prepare this legislation the need to spell out this tenth specific objective was overlooked.

However, the language of this new specific objective still refers to recovery of the economy. If the new specific objective focuses the ERI spending on recovery interventions that at the same time further the green transition, then it could imply that much more than 30% of the additional expenditure would be devoted to environmental and climate-related spending. But until we see the text of this new specific objective, as well as Commission guidance on what interventions Member States can fund under the ERI in their CAP Strategic Plans, we cannot be sure.

Conclusions

Within the context of a significantly reduced volume of resources for the ‘standard’ MFF as compared to its original MFF proposal in May 2018, the Commission has added an additional €24 billion in constant 2018 prices (€26.5 billion in current prices) to the CAP budget. This is made up of €4 billion extra for Pillar 1, €5 billion extra in the MFF for Pillar 2, and a further €15 billion for Pillar 2 under the ERI.

The additional Pillar 1 commitments are earmarked for market-related expenditure and to bolster the EU’s crisis management capacity in agriculture. No change is proposed in the direct payment ceilings set out in Commission’s May 2018 proposal. It is worth noting that President Michel, in the second draft of his negotiating box at the European Council’s February 2020 meeting, proposed to increase the direct payments ceiling by €2 billion (€1.5 billion from the Heading 3 margin and €0.5 billion by switching funds from CAP market promotion measures). The Commission’s new proposal could still be amended by the European Council to increase direct payment ceilings though I would view this as unlikely.

With the additional assigned revenue from the ERI, EAFRD funding in Pillar 2 is now cut by less in constant 2018 prices/increased by more in current prices than EAGF spending in Pillar 1, thus reversing the priorities between the Pillars in the Commission’s original proposal. The Commission has also maintained its co-financing proposal whereby national governments will increase their contribution to EAFRD spending by 10 percentage points.

However, there does appear to be a potential mismatch between the great bulk of the additional EAFRD funding deriving from the ERI, which has to be committed within the first three years and which has recovery from COVID-19 as it main priority, and the longer-term need to provide funding to support farmers in the green transition. In this context, the Commission’s conversion to the idea of a mandatory minimum ring-fencing of eco-schemes in Pillar 1 could be an important commitment.

Analysis of the CAP budget numbers shows that there is a small (5%) cut in the volume of resources in constant price terms compared to the final year of the current MFF, but a small increase (2%) in current prices. However, if current price amounts are increased each year by 2% but inflation remains subdued at 1% per annum over the programming period, the real value of payments to farmers will be maintained. This conclusion is only strengthened if the focus is put on total transfers to farmers and not just the EU transfer by factoring in the additional national contribution to EAFRD spending proposed by the Commission.

This post was written by Alan Matthews

Update 4 June 2020. CAP share figures in column G in the first table changed to reflect share in reinforced MFF alone, excluding ERI.

Dear Alan, this is an excellent analysis and presentation of this very political sensitive issue.

Congratulation,

Emil Erjavec