In the early hours of Tuesday 21 July 2020, around 5.30 am, after four days and nights of negotiations, European Council leaders reached agreement on both the Next Generation EU recovery instrument and the Multi-annual Financial Framework (MFF) for the period 2021-2027. Reaching unanimous agreement among 27 leaders who entered the negotiations with widely different positions was an astounding political achievement. And although the inevitable compromises were accompanied by expressions of regret, it is extraordinary that every leader has expressed satisfaction with the final outcome.

There are many aspects of the European Council conclusions that warrant analysis: the agreement that the EU for the first time can issue debt to fund a stimulus package to address the catastrophic economic fall-out from the coronavirus pandemic; the future links between EU financial transfers to countries and the rule of law; the framework set out for additional own resources in the coming years; the continued relevance of budget rebates: and the extent to which the final outcome succeeded in ‘modernising’ the budget to reflect the EU’s new priorities.

In this post I concentrate on what the final outcome implies for the CAP budget in quantitative terms. The outcome is not what farmers had hoped for but nor is it as bad as they feared.

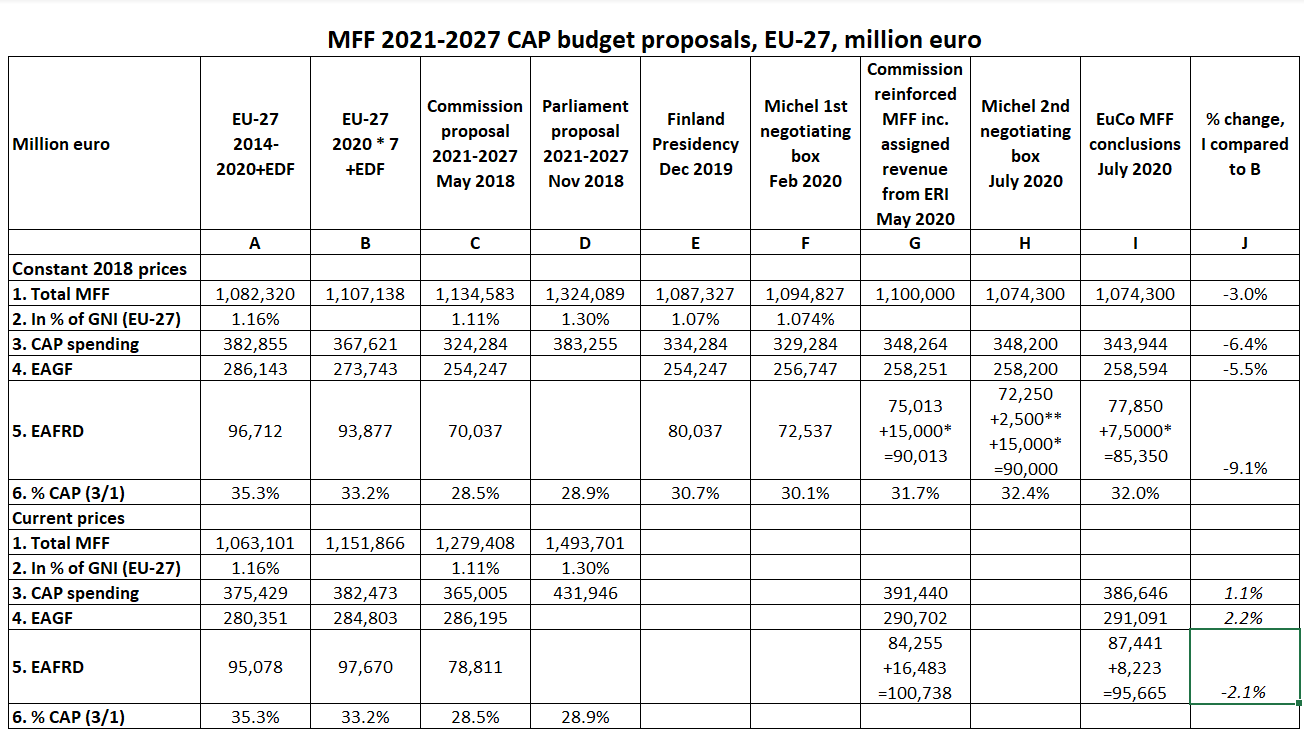

The following table shows how the proposed CAP budget evolved in successive iterations of the MFF negotiating box.

Notes: * Contribution to EAFRD from Next Generation EU recovery instrument; ** €2.5 billion of the EAFRD total was held back as unallocated. The current price figure for the CAP EAGF spending is from EUCO 10/20, the EAFRD figure is the sum of the EAFRD MFF total provided on the Commission MFF webpage plus half of the current price Next Generation EU assigned revenue notified in COM(2020) 459, and the total CAP figure in current prices is the sum of these two.

The overall CAP budget

The MFF negotiations were kicked off by the Commission proposal in May 2018. The European Parliament responded with its own alternative MFF proposal in November 2018. The first negotiating box with figures was presented at the end of the Finnish Presidency in December 2019. This was followed by European Council President Michel’s ill-fated version of the negotiating box presented prior to the European Council meeting in February 2020.

The political landscape changed dramatically in March 2020 when the coronavirus pandemic took hold and Member States began to lock down their economies to slow its spread. As economic activity collapsed, the need for a European-level stimulus package became evident. On May 18, France and Germany proposed a €500 billion stimulus package to be funded by EU borrowing. On 27 May, the Commission followed up on this with a new budget proposal built on two legs: a €750 billion European Recovery Instrument (ERI) called Next Generation EU, and a proposal for a ‘reinforced MFF’ including ideas for new own resources. This formed the basis for President Michel’s second negotiating box circulated prior to the most recent European Council summit. Various changes were made to this during the four days of negotiations, resulting in the final European Council agreement.

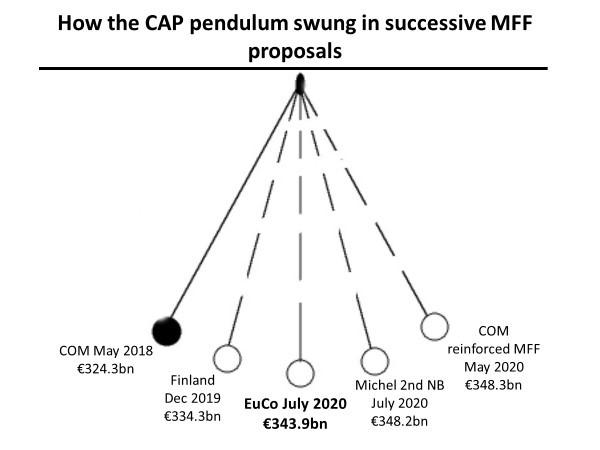

The CAP budget figures swung to and fro like a pendulum during these successive iterations of the MFF budget. The Commission’s original proposal was for a CAP budget of €324.2 billion (all figures in constant 2018 prices). This was increased to €334.3 billion in the Finnish negotiating box and reduced to €329.3 billion in Michel’s first negotiating box. The CAP budget got a boost in the Commission’s reinforced MFF to €348.3 billion thanks mainly to an allocation of €15 billion from the European Recovery Instrument. This was cut back slightly to €348.2 billion in Michel’s second negotiating box, and finally landed at €343.9 billion in the European Council conclusions.

There has been a lot of focus on how the outcome compares to the allocation to the CAP in the current MFF period 2014-2020. As explained in this previous post, there are different ways to make this comparison. Two estimates of what is meant by ‘MFF spending 2014-2020’ are shown in Columns A and B in the previous table, respectively, with the Commission’s preferred approach being Column B. Column B refers to a baseline for commitments in the current MFF derived by taking commitments in the final year (2020) and multiplying by seven, rather than simply summing up commitments in each of the seven years as shown in Col. A. On either comparison, the outcome implies a reduction in constant 2018 prices, by either 10.2% relative to Column A (€38.9 billion) or 6.4% relative to Column B (€23.7 billion).

The table also shows the comparison in current prices. While the European Council conclusions provide the EAGF total in current prices, the EAFRD figure is the sum of two items. EAFRD spending in the MFF in current prices is based on this table provided on the Commission’s MFF webpage. The additional assigned revenue from the Next Generation EU recovery instrument is based on the current price figures in the Commission’s draft legislative proposal, but divided by two as the European Council reduced the Commission’s original EAFRD amount by half. In broad terms, the CAP budget has been maintained in nominal terms, and even slightly increased, compared to the 2014-2020 baseline.

It is also worth highlighting the difference between the European Council outcome and the Commission’s original MFF proposal in May 2018. Here there has been a clear increase amounting to almost €20 billion in constant 2018 prices.

Pillar 1 CAP budget

The European Council outcome represents a small increase over the EAGF Pillar 1 budget proposed by the Commission in May 2018. The breakdown of this increase between direct payments and market-related expenditure is shown in the following table. There has been a small increase in the amount allocated to direct payment envelopes, but a small decrease in the amount allocated to market-related expenditure.

Breakdown of Pillar 1 commitment appropriations, constant 2018 prices, million euro

| Commission MFF proposal May 2018 | EuCo MFF conclusions July 2020 | |

| Direct payments | 235,022 | 239,916 |

| Market-related expenditure | 19,225 | 18,678 |

| Total EAGF Pillar 1 | 254,247 | 258,594 |

The increase shown for direct payments implies that the relevant Annexes II and III in the CAP transition regulation and in the draft CAP Strategic Plans regulation which give the direct payment envelopes by Member State each year in current prices will be changed. The new allocations will also need to take into account the impact of the further move towards external convergence agreed in the European Council conclusions which will start in financial year 2022. Given the slight increase in the current price value of direct payments in the next MFF shown in the first table, there should be sufficient funds in the 2021 budget to fund the national envelopes and payments to farmers foreseen in the amended direct payments regulation No. 1307/2013 without recourse to the financial discipline mechanism.

There is a reduced allocation for market-related expenditure. Part of this is pre-allocated to Member States for sectoral interventions while part is used for measures such as promotion and school schemes. When the Commission increased the EAGF allocation by €4 billion in its reinforced MFF proposal compared to its original May 2018 proposal, it justified this by saying that this money is intended for “Strengthening the resilience of the agri-food and fisheries sectors and providing the necessary scope for crisis management”. In a previous post, I suggested that this additional funding could help to cover the €1 billion safety net promised by former Agriculture Commissioner Phil Hogan to address potential market disruption if the EU-Mercosur Free Trade Agreement enters into force. There is no specific mention of this safety net in the European Council conclusions and one must assume it has vanished into the far distance along with the Commissioner.

However, a relevant factor for agricultural crisis management not shown in the European Council conclusions is the margin left in Heading 3 in the MFF between committed expenditure and the Heading 3 ceiling. This margin can potentially be available for agricultural crisis management.

Further, the creation of a new special Brexit Adjustment Reserve worth €5 billion in constant 2018 prices (€5.3 billion in current prices if all of it is spent in 2021) to counter adverse consequences in Member States and sectors that will be worst affected should be highlighted. This was particularly pushed by Ireland whose agri-food sector stands to lose the most when the current Brexit transition period ends at the end of this year. The criteria by which this crisis reserve will be disbursed are not yet known and the Commission is invited to bring forward proposals by November 2020. However, a significant chunk of this money will likely be directed to farming in Ireland and in other Member States given its exposure to negative impacts.

Pillar 2 CAP budget

There have also been interesting dynamics behind the European Council conclusions on the EAFRD allocation for rural development. In the Commission’s original MFF proposal, the EAFRD budget was cut much more severely than the EAGF budget. Rural development programmes are co-financed by Member States. Some of this reduction in EAGF spending was compensated by a reduction in EU co-financing rates which would require Member States to put up more of their own money in order to draw down EU funds.

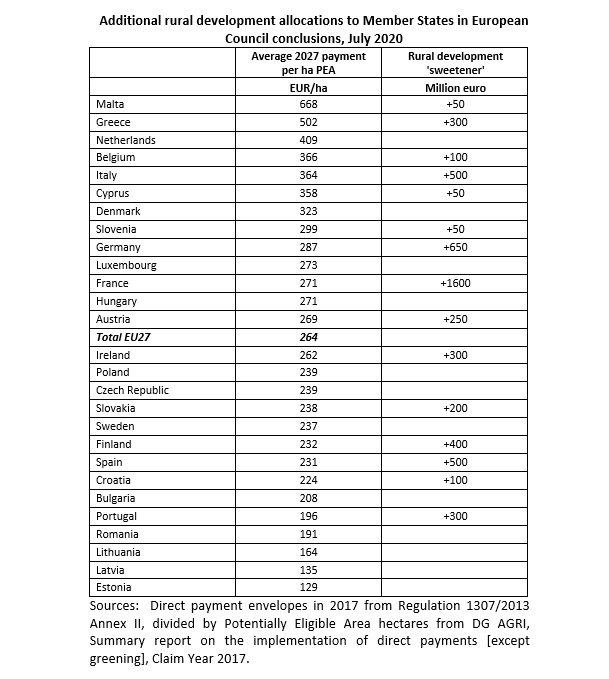

The Finnish Presidency restored some of the reduction by adding €10 billion to the EAFRD budget, but most of this increase was removed in Michel’s first negotiating box. The fortunes of rural development programmes were dramatically altered when the Commission proposed in its reinforced MFF to boost rural development spending by a further €15 billion from the Next Generation EU recovery fund. This level of funding was broadly retained in Michel’s second negotiating box, with one crucial qualification. Michel, following former European Council President von Rompuy’s playbook in 2013 for successful MFF summitry, decided to withhold €2.5 billion of EAGF funding as potential ‘sweeteners’ to win over waverers to a final deal. Finally, in the hectic four days of negotiations, this pot of ‘sweeteners’ was further increased. By Saturday evening, it had been increased to €4.6 billion and by Tuesday morning a further €750 million had been found to increase the pot to €5.35 billion shared between 15 countries.

According to the European Council conclusions, this money is intended for Member States facing particular structural challenges in their agriculture sector or which have invested heavily in Pillar II expenditure or which need to transfer higher amounts to Pillar I so as to increase the degree of convergence. In the light of the last criterion, the next table shows the countries benefiting from ‘sweeteners’ ranked according to their direct payment per hectare in 2017.

While a range of criteria are mentioned as contributing to the justification for these ‘sweeteners’, there is a slight bunching at the top of the table. These are the countries that expect to lose out from further external convergence of Pillar 1 payments. France emerges as the clear winner with an extra allocation of €1.6 billion over the MFF period. Compensating these countries through higher rural development allocations may have been an implicit objective in the allocation of ‘sweeteners’. However, the ‘base’ amount allocated to the EAGF budget before sweeteners and before the ERI injection of €7,500 million is still higher than the original EAFRD allocation in the Commission’s May 2018 proposal. The latter formed the basis for Member State individual rural development envelopes in the draft CAP Strategic Plan Regulation. So all Member States will see a small rise in their national envelopes compared to the figures in that draft Regulation, with somewhat bigger increases for the 15 beneficiaries of President Michel’s largesse. There will also be further additions when the allocations from the ERI injection are known.

Pillar 2 co-financing

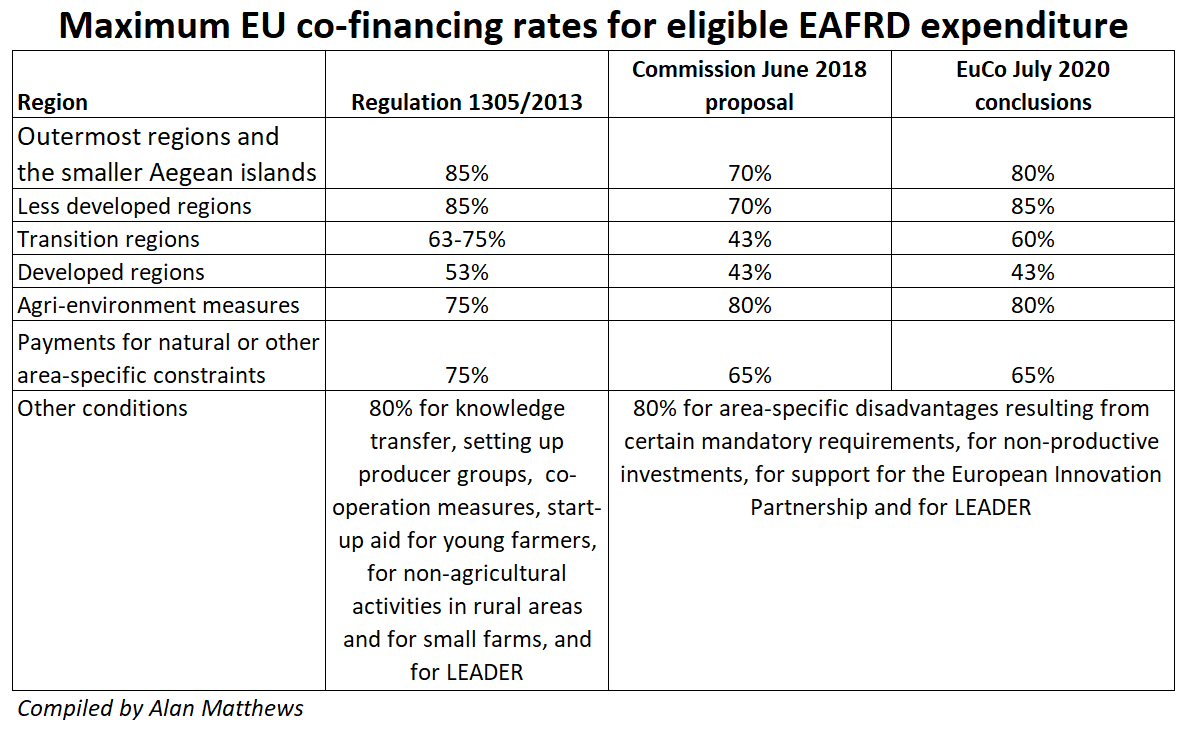

Another important change in the Pillar 2 arrangements are the EU co-financing rates. The Commission’s May 2018 MFF outline proposed to lower co-financing rates across the board (except for agri-environment-climate measures, see following table). This would mean that Member States and regions would be required to put up more of their own money in order to draw down EAFRD funds. The argument in favour of this was that it would help to offset some of the proposed reduction in the EAFRD budget and increase overall rural development funding. The argument against was that, for some Member States and regions, budget constraints could make it difficult to find the additional national co-financing and might mean that they would be unable to draw down all the EU funds to which they were entitled.

The European Council conclusions altered the Commission’s proposal in important ways although they maintain the fundamental approach. The maximum EAFRD contribution rate is reduced to 60% of eligible public expenditure in transition regions and to 43% in developed regions. However, the rate is maintained at 85% for the less developed regions. Furthermore, the higher rate of 80% is maintained for agri-environment-climate expenditure, giving Member States and regions an incentive to prioritise spending in this area if they wish to minimise their own budget contribution. The overall outcome will be to attract additional national financing for EAFRD-funded interventions in the national CAP Strategic Plans, though the precise magnitude of this additional funding will not be known until these Plans are finally approved.

Conclusions

This post examines what the historic European Council conclusions on the Next Generation EU fund and the MFF 2021-2027 agreed earlier this week imply for agricultural spending in the coming years.

The farm unions and their political representatives in COMAGRI in the European Parliament have argued that the greater environmental and climate ambition envisaged in the CAP post 2020, and the goals for the green transition set out in the Farm to Fork and Biodiversity Strategies, require additional financing. They have called for the CAP budget to be maintained in constant prices relative to the 2014-2020 MFF period. As the first table in this post shows, this has not happened.

Depending on whether the comparison is made with the overall volume of resources allocated to the CAP in 2014-2020 (Column A) or the imputed volume derived from the 2020 calendar year allocation multiplied by 7 (Column B), there is a reduction of either €39 billion or €24 billion in constant prices (either 10% or 6%).

However, the European Council outcome maintains the CAP budget in current prices, or even slightly increases it, compared to 2014-2020 expenditure. It also represents a significant increase of almost €20 billion in constant prices compared to the Commission’s original proposal in May 2018. Furthermore, overall CAP budget expenditure includes national expenditure on rural development programmes. Additional national expenditure will be generated by the average reduction in EU co-financing rates.

Indeed, there will be pressure on national governments to further top-up rural development spending as is possible under EU state aid rules, as evidenced by this reaction from the Irish Farmers’ Association to the budget deal. The importance of national spending has been underlined in the responses to the COVID-19 crisis. In any case, as I argued in a previous post, constant price figures (converted to current prices using a fixed deflator of 2% per annum) are not necessarily a good guide to future expenditure in real (deflated) terms if the actual rate of inflation over the coming period is less than 2%.

As well as these quantitative elements, the European Council conclusions cover other CAP elements, including external convergence, capping, the agricultural reserve, flexibility to transfer resources between Pillars, and climate mainstreaming, which we will return to in another post.

The European Council conclusions are not yet a done deal. The consent of the European Parliament is needed as is approval by national parliaments (for the Own Resources Decision). The Parliament’s initial reaction welcomed the agreement on the European Recovery Instrument but found it unacceptable that the long-term budget has been cut. The Council will now finalise its mandate to enter negotiations with Parliament while the Parliament will also need to agree its position before starting negotiations with the German Presidency of the Council as soon as possible.

This post was written by Alan Matthews.

Update 22 July 2020. An explanation of Columns A and B in the first table has been added.

Update 24 July 2020. The text has been corrected to point out that it is not likely the financial discipline mechanism will be used to reduce 2020 direct payment national envelopes.

Update 12 Sept 2020. The figures for the CAP budget in current prices have been updated with the Commission estimate for EAFRD spending communicated to COMAGRI on 7 September 2020 by Commissioner Wojciechowski and the text has been amended accordingly.

Update 8 October 2020. The figures for the CAP budget in current prices were again revised taking account of information published on the Commission’s MFF webpage on 28 September giving EAFRD spending in the MFF in current prices.