Let me make clear immediately that I have taken this headline from an article published in Politico yesterday written by Giorgio Leali and collaborators immediately following the conclusion of the informal summit of EU leaders in Cyprus 23-24 April. The article goes on to identify as a problem: “They still don’t agree on what it should do, how big it should be, or who should pay for it.” This rings very true.

So far, we have just two proposals for the size of the 2028-2034 MFF on the table. The first is that of the Commission. Shortly before the European Union leaders met, the Budget Committee of the European Parliament came up with its Interim Report on the next MFF. This sets out the Parliament’s view on the appropriate size of the next MFF. This will be voted on in plenary by the Parliament on 29 April and, once confirmed (which will almost certainly be the case), the Parliament will be ready to enter into discussions with the Council once it has agreed on its common position. For this reason I refer to this as the Parliament’s view in this post. The Council’s position will not become clear until at the earliest June 2026 when the Cyprus Presidency will present a first version of the ‘negotiating box’ to the June 2026 meeting of the European Council.

In this post, I look at the ambition in the Commission and Parliament proposals relative to the size of the current 2021-2027 MFF. I underline the quantum leap embodied in these proposals, and argue that the final outcome will almost certainly be a smaller figure.

The Parliament’s MFF role

First, a short reminder of the Parliament’s role in the process of establishing the MFF. Since the Lisbon Treaty entered into force, the Parliament must give its consent for the Council’s regulation on the MFF to be adopted. It can only accept or reject the MFF as a whole, it cannot change specific spending lines or figures. Because of this consent requirement, the Parliament has a veto power. It uses this leverage to force the Council to negotiate, allowing it to influence the final package despite the lack of formal amendment rights. If no agreement on the MFF is reached, the spending ceilings and provisions from the last year of the current MFF are automatically extended until a new deal is reached (Article 312(4) TFEU).

For this reason, the Parliament’s views can impact on the final outcome. The negotiations on the 2014-2020 MFF were the first MFF negotiation since the Lisbon Treaty granted the Parliament the power of consent. In March 2013 the Parliament voted overwhelmingly to reject the deal reached by the European Council the previous month. Skilful negotiations under the Irish Presidency led to various concessions (the Council agreed to an amending budget to pay off unpaid bills from previous budgets, it agreed to allow unused funds to be shifted between years and categories, and it agreed to a mid-term review), ultimately leading to Parliament giving its consent in June 2013.

Similarly, the Parliament in July 2020 criticised the European Council’s political agreement on the MFF earlier that month. This was the agreement that initiated the Next Generation EU loan package in response to COVID-19. It then fell to the German Presidency to lead trilogue negotiations with the Parliament. This led to the Council agreeing to an additional €15 billion for flagship programmes for Erasmus+, Horizon Europe and EU4Health, a stronger link between EU funding and respect for the rule of law (Conditionality Regulation), and agreeing a legally-binding roadmap to introduce new ‘own resources’ to repay the pandemic recovery debt. With these concessions, the Parliament gave its consent in December 2020.

The current state of play

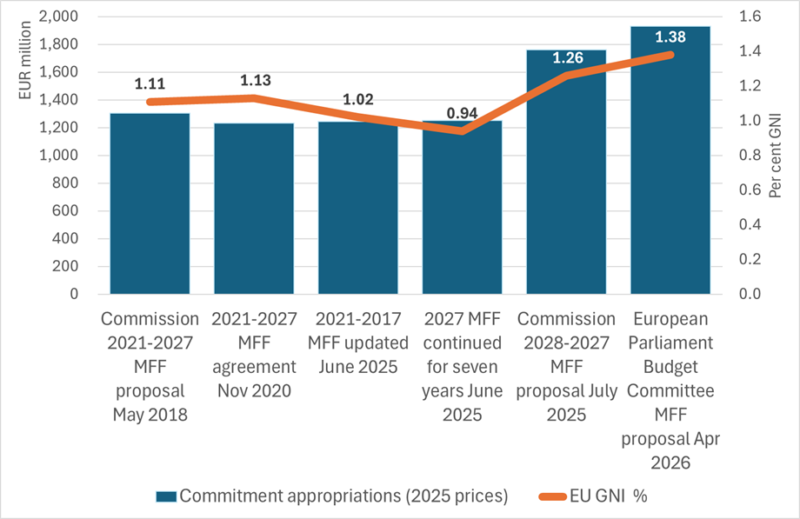

A comparison of the Commission and Parliament proposals with the current MFF illustrates the extent of ambition that they involve, and why it must be deemed unlikely that either will fly. This is not a normative judgement on my part. I think there are good arguments for a larger EU budget. But we also need to understand the fiscal constraints now faced by nearly all EU Member States. I illustrate the scale of the fiscal demands implied by the Commission proposal and, even more so, the Parliament position in the following chart (Figure 1).

Sources: The Commissions May 2018 proposal COM(2018) 321; EPRS EU budget 2028-2034 for Nov 2020; Updated 2021-2027 MFF and 2927 MFF continued in June 2025 from COM(2025) 800; Commission MFF proposal July 2025 COM(2025) 571; EP Budget Committee Apr 2026 Report – A10-0105/2026. Figures for the 2021-2027 MFF in 2018 prices have been converted to 2025 prices by multiplying by 1.1487 (=(1.02)*7).

The chart compares the 2021-2027 MFF proposal and outcomes with the two proposals to date for the 2028-2034 MFF. We first look at the absolute size of the MFF. The Commission 2018 proposal was for an MFF corresponding to commitment appropriations of €1,303.3 million in 2025 prices. The final MFF agreement (including the MFF mid-term review) led to a reduction in the Commission proposal totalling €1,246.6 million in 2025 prices. In the most recent technical adjustment to the MFF (an annual exercise where the Commission updates the MFF figures to take account of the most recent estimates of EU GNI) published in June 2025 the MFF figure remained unchanged (the reported figure is slightly smaller at €1,244.0 million converted to 2025 prices but this may reflect rounding errors due to the timing of commitments over the MFF period). I have also calculated an MFF total assuming that the commitment appropriations agreed for 2027 were maintained for a seven-year period. This would give an MFF budget equal to €1,252.5 million in 2025 prices, so not that different from the official figure.

We can now evaluate the increases proposed by the Commission (to €1,763.0 million in 2025 prices which includes the repayment of the NGEU borrowing) and the Parliament’s position which is an MFF of €1,931.8 million in 2025 prices (again, including repayment of the NGEU borrowing of €149.3 million in 2025 prices – the Parliament calls for this repayment to be kept outside the MFF ceiling but it will still require resources transferred either directly or indirectly from Member States to finance it).

The Commission proposal represents a 41% increase over the current MFF (29% in real spending if the NGEU repayment is excluded), while the Parliament’s position would require a 55% increase (43% in real spending if the NGEU repayment is excluded). Excluding the NGEU repayments, the Parliament increases real spending in the MFF budget compared to the Commission proposal by 10%. Of course, it does not have to find the money to pay for this expenditure.

We can also compare what the two MFF proposals for the 2028-2034 period mean as a percent of EU GNI compared to the current MFF. The EU economy has grown since the last MFF, so we would expect the percentage share increases to be lower than for the absolute amounts.

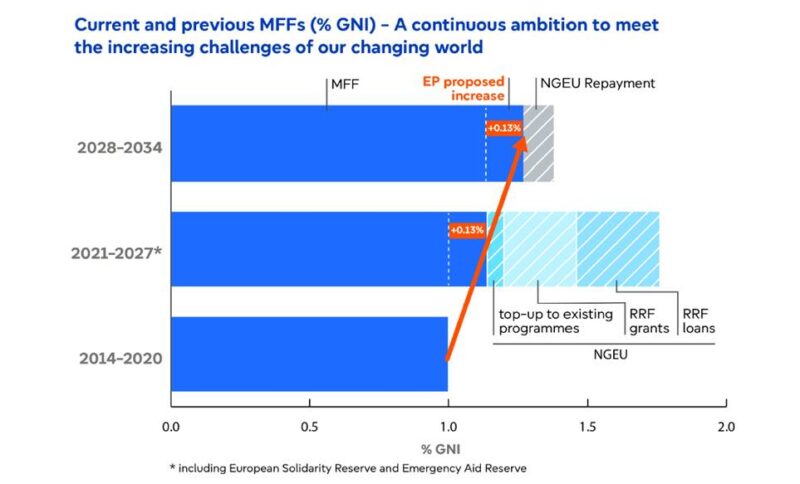

Here the Parliament’s press service has included a figure (shown as Figure 2 below) which suggests that its 2028-2034 MFF proposal continues the smooth upward trend in the share of EU GNI initiated in the current MFF. This is only the case if we discount the NGEU repayment, as is shown in Figure 2. But the Parliament’s diagram also presents a misleading picture if viewed from the perspective of Member States. This is clear if we return to look at the evolution of the EU GNI MFF share over time, shown in Figure 1.

Source: European Parliament press release ‘EU long-term budget: MEPs want a 10% increase to support EU priorities’, 15 April 2026.

Figure 1 shows that the Commission’s MFF proposal was expected to land at 1.11% of EU GNI when it was published in 2018. This was a significant increase from the 1% figure in the previous MFF, in part reflecting the withdrawal of the UK from the EU. This meant the loss of a significant net contributor to the EU budget, requiring a general increase in contributions from remaining Member States simply to maintain the previous level of expenditure. Although the final MFF outcome was a little smaller than the Commission proposal, its share of EU GNI when it was agreed in December 2020 (and after adjusting for the mid-term review) increased to 1.13% of EU GNI. This was due to a downward revision in EU GNI growth estimates following the onset of the COVID-19 lockdown in March 2020.

By 2025, this EU GNI share had fallen further to 1.02%. This was because the 2% deflator used to adjust the MFF ceilings each year in current prices was below actual inflation in the early years of the MFF. Thus, nominal GNI increased more rapidly than what the Commission had projected at the start of the MFF, and the real burden of MFF spending fell (see the calculations in the Commission Staff Working Paper accompanying its MFF Communication SWD(2025) 570). In fact, in 2027, the Commission’s latest technical adjustment of the MFF projects that Member States will only be required to contribute 0.94% of their GNI to finance the EU budget in that year. This follows the general tendency for the share of MFF commitments as a share of EU GNI to fall over the course of an MFF as the annual expenditure for many MFF headings is held constant either in real or even nominal terms, while EU GNI increases.

Against this background, we can now assess the projected share of EU GNI needed to finance the Commission’s and Parliament’s MFF proposals for 2028-2034. For the Commission, the figure is 1.26% and for the Parliament it is 1.38% (including the NGEU repayment in both figures).

The Parliament Press Office diagram (shown as Figure 2) makes it appear that the share of EU GNI required to finance the EU budget increases from 1% in 2014-2020, to 1.13% in 2021-2027, to 1.26% in 2028-2034 (in fact, the Parliament proposal is for an MFF of 1.27% of EU GNI if the 0.11% share for the NGEU repayment is excluded).

For Member States, however, the increase will be seen more as an increase from 1.02% (the share now assessed in the current MFF) to either 1.26% or 1.38%. Inded, if the projected 2027 figure for the share of EU GNI to be committed to the EU budget of 0.94% is taken as the starting point, the increased demand on Member State resources would be even greater. I find the likelihood of increases of this magnitude implausible.

Conclusions

The Parliament’s proposed MFF budget would imply a 55% increase in EU spending in real terms in the next MFF compared to this MFF. There are good reasons to argue that, given the scale of the challenges that the EU faces, a budget of this size could be justified. But the prospects of Member States finding the resources to fund such a budget are likely non-existent.

The problem with the Parliament’s role is that, under the Lisbon Treaty, it does not have to take responsibility for its MFF proposals. It has the power to veto the Council proposal, but it is not required to raise the money to finance its own proposal. This leads to a situation where the Parliament accedes to the demands of each interest group by simply aggregating them into an ever-larger total. For this reason, it is not a serious player in the budget negotiations, although the requirement to get its consent means that its views cannot be ignored. On the Council side, on the other hand, leaders must reach agreement on the size of the MFF by unanimity. The important reason for this is that this agreement also commits each leader to return home and ensure the passage of the Own Resources Decision which provides the finance according to their constitutional requirements. In the majority of countries this means that parliamentary approval is needed (and, in the case of Belgium, also its regional parliaments) while in a minority of countries the decision can be made by the government.

This lack of balance between the Parliament’s tax-raising and spending powers has been tolerated by pro-Europe voices to date because it is evident that a larger EU budget would be desirable. So EU supporters have acclaimed the Parliament’s position seeking a larger budget without questioning this larger imbalance. But it is clear that only those who are required to raise the money are in a position to balance competing demands when it comes to deciding on the level of expenditure.

So we wait to see what the Council’s opening gambit will be. The remarks by the European Council President António Costa at the press conference following the informal meeting of heads of state or government of 23-24 April 2026 were rather downbeat and did not suggest significant progress had been made. The full quotation is as follows:

This morning, we had an exchange on our next long-term budget (the so called Multiannual Financial Framework). We have a collective responsibility to reach an agreement by the end of the year. Only this way can we make sure that the next MFF hits the ground running from the beginning of 2028. Matching our ambitions with the necessary resources will be key.

Our debate today confirmed that New Own Resources will have to play an important role to fund the budget. There is still work to be done. The Commission’s New Own Resource package proposal will continue to be the basis for this further work – and there was also openness to consider other proposals, namely those put forward by the European Parliament. Our discussion provided important guidance for the next steps. We will return to the MFF discussion in June, on the basis of a first proposal with figures prepared by the Cypriot Presidency.

Given that the fiscal pressures on Member States in 2026 are at least as strong as in 2020, I do not see even the Commission MFF proposal surviving at the level proposed. What will be interesting is where the cuts will be made. Will reductions be made in the EU’s traditional priorities (covered by the funding allocated to the National and Regional Partnership Fund (NRPF) including the CAP, or will they be made to the European Competitiveness Fund and Global Europe which is where the large increases in the budget are proposed (you can take it as given that the fourth MFF heading, Administration, will be cut but it is not a major part of the budget).

The NRPF is pre-allocated to Member States, so each country can calculate its net position. For this reason, there will be strong resistance to cutting further spending on traditional priorities. So, despite all the brave talk about equipping the Union to address new priorities, such as defence, competitiveness and the green transition, Member States will more likely accept cuts in these areas because they do not see explicit losses in terms of receipts (what Member States receive is not known in advance). We may not like it, but this is how the sausage-making machine that is the EU MFF budget negotiations works.

This post was written by Alan Matthews.

Photo credit: Kirsebærallee, Bisbebjerg, Copenhagen, own photo.