Two events in the previous week give us a much clearer idea of what to expect for the CAP budget in the Commission’s proposal for the next Multiannual Financial Framework (MFF) at the end of May. Of course, the Commission’s proposal is only the start of the MFF negotiations. The MFF must ultimately be agreed unanimously by all Member States and (for the own resources decision) by their national parliaments, and also gain the approval of a majority in the European Parliament. Much can happen between the initial proposal and the final Council conclusions.

The two events in the previous week were Budget Commissioner Oettinger’s speech setting out his approach to the MFF proposal at a meeting in Brussels organised by the European Political Strategy Centre, the Commission’s in-house think tank, and his comments following the first presentation of his ideas to the Commission College.

Commissioner Oettinger states that he expects to make cuts of between 5-10% in both CAP and cohesion funding. Based on these comments, the good news for the agricultural sector is that the CAP budget will be broadly maintained in nominal terms, which would be the same outcome as for the current MFF. Or, to put it another way, it now seems unlikely that budget pressures will be a driver of any major CAP changes in the next period. Those interested in the main message of this post need read no further. What follows is my attempt to explore the implications of Oettinger’s comments in more tedious detail.

The reconciliation of this apparent contradiction is that direct payments which make up more than 70% of the CAP budget are not indexed to inflation. They are fixed in nominal terms, and thus fall in real terms in the MFF given that the Commission assumes an annual 2% rate of inflation each year. This alone means that the CAP budget will fall by over 5% in real terms in the next MFF, even if Pillar 2 spending is held constant in real terms and without any cut in the nominal amounts for Pillar 1.

Oettinger’s budget parameters

These are the main points in Commissioner Oettinger’s approach to the next MFF:

• The MFF will be for a seven year period (moving to 5 year periods for the MFF after next).

• The MFF has to address two main financial gaps, one on the revenue side caused by the departure of the UK which is a major net contributor to the EU budget, and one on the expenditure side to fund new priorities which were not envisaged or foreseen at the start of the current MFF.

• The Brexit financing gap is estimated at €13 billion annually, which Oettinger proposes to close 50% by making savings in existing programmes, and 50% from ‘fresh money’ from the remaining EU-27 Member States. This would require an additional €6.5 billion annually in additional contributions.

• For the new priorities, Oettinger proposes that these should be financed 20% by making savings in existing programmes, and 80% from ‘fresh money’ from the remaining Member States.

• Proposed Member State contributions to new programmes (refugees, fight against terrorism, security and defence) will be around €10 billion annually, suggesting total expenditure on these new priorities of €12.5 billion (assuming the 20:80 financing key).

• We can derive the expected savings in traditional policies as €6.5 billion annually to cover the Brexit shortfall plus a further €2.5 billion to be switched to new priorities (this is 20% of the total spend of €12.5 billion on new priorities), for a total of €9 billion savings annually. As total new spending on new priorities is €12.5 billion, this implies a relatively small increase in the total size of the MFF of around €3.5 billion annually.

• The shares of the CAP and cohesion policy will fall from around 35% each in the current MFF to around 30% each in the next MFF. Cuts will be ‘reasonable’, possibly of the order of 5-10%. However, there will be no cuts in either the Horizon post 2020 research or ERAMUS+ student and young people exchange programmes.

• Commissioner Oettinger has requested Member States to enter into negotiations as soon as the Commission publishes its proposal, with a view to reaching a decision by February 2019. This would allow the European Parliament to approve the MFF before its current session comes to an end in March. The feasibility of this timeline can, of course, be questioned, but Commissioner Oettinger cannot be faulted for lack of ambition.

Commissioner Oettinger has also made some proposals on the financing or revenue side of the budget:

• He argues that there is a need to raise the ‘political ceiling’ which limits the share of EU budget commitment appropriations to 1% of EU Gross National Income (GNI). (I discuss the background to this political commitment, which was originally stated in terms of payment appropriations, in this earlier post). He talks in terms of an EU budget which would amount to 1.1x% of EU GNI, that is, somewhere between 1.1% and 1.2% of GNI.

• New sources of revenue will be proposed, and he has specifically mentioned the proceeds from auctioning emissions allowances in the Emissions Trading Scheme and a tax on plastics (though apparently he had not run this latter idea past his fellow Commissioners before launching it, and the Commission has quickly retreated from this idea).

• All rebates should be ended.

Based on these parameters, it is possible to put together an MFF which fits these targets. This is a very speculative and approximate exercise, but it helps to identify some of the key decisions. To prepare this outline of the Commission’s MFF proposal, I make some further assumptions:

• A number of instruments are available outside the expenditure ceilings agreed in the 2014-2020 MFF (e.g. Emergency Aid Reserve, European Union Solidarity Fund, Flexibility Instrument and others). It is assumed they are either included in the next MFF as part of the new priorities or continue to be funded outside the MFF. Either way, they are not considered further.

• Commissioner Oettinger has put absolute figures on the two financial gaps, but it is not clear how these are defined or what units they are measured in. For the purpose of constructing a speculative MFF, I assume that these figures are in 2020 prices and they represent the average annual amounts over the next seven-year MFF period. The annual figures could be lower at the beginning of the next MFF period and be greater towards the end. Rather than try to guess a schedule of commitments, I choose to work with the mid-year 2024 as the representative average year for the whole period. This means that the MFF total for the seven-year period is obtained by simply multiplying the 2024 figure by seven.

doub• Similarly, Commissioner Oettinger has stated that he intends to maintain expenditure on ERASMUS+ and Horizon post 2020 programmes. But it is not clear if he intends to maintain these programmes at their levels in the current MFF (which includes the UK) or whether he intends to maintain spending levels for the remaining EU-27 Member States. Because the UK can make voluntary contributions to these programmes if it wishes to continue to participate in them after Brexit, I choose to interpret Mr Oettinger’s commitment as maintaining expenditure levels for the remaining EU-27 Member States.

• I choose to present the MFF expenditure headings in 2020 prices, although the Commission proposal in May will probably be made in 2018 prices.

A speculative Commission MFF proposal

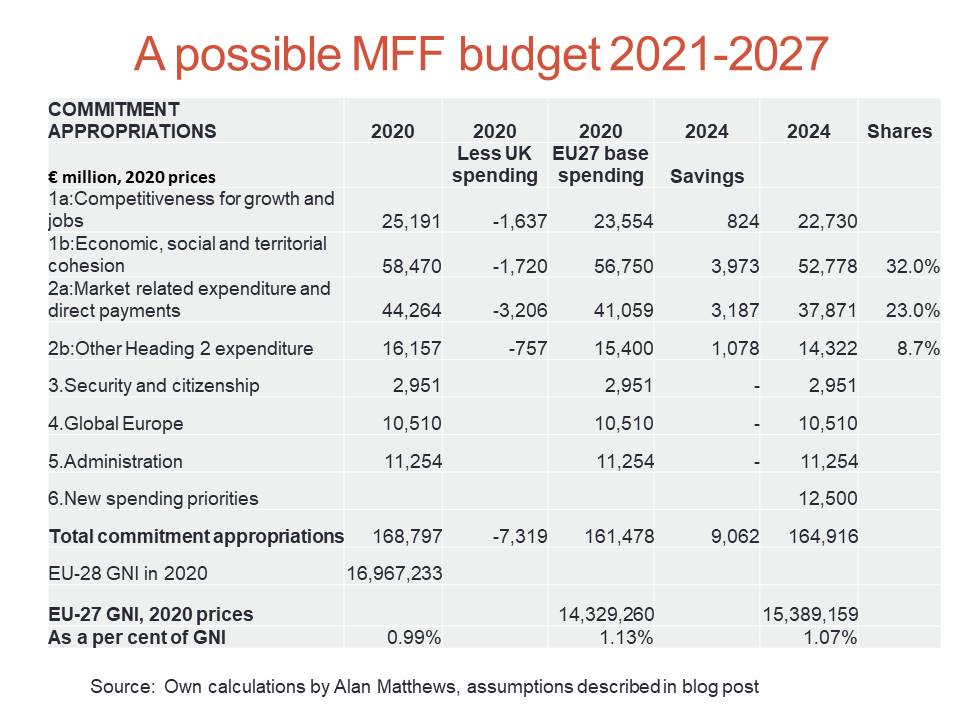

Based on these assumptions, my speculative Commission MFF proposal in commitment appropriations is shown in the table below (click on the table for a better view). The starting column shows the MFF figures for the last year of the current MFF (2020) which is taken from the Commission’s Technical adjustment of the financial framework for 2018 in line with movements in GNI (ESA 2010).

In the next column, I deduct the estimated UK share of pre-allocated commitments in 2020 as these will not be carried forward as a charge into the next MFF. UK commitments for CAP Pillar 1 and Pillar 2 expenditure for each year in the MFF are set out in the CAP regulations. For cohesion fund spending, I have conservatively estimated 2020 commitments in the UK by dividing the UK’s seven-year MFF allocation equally across years – this figure is close to the average payment appropriations paid to the UK in the years 2014-2016 converted to 2020 prices.

Funds under the ‘Competitiveness for growth and jobs’ heading are not pre-allocated but the UK has been successful at drawing down funds under this heading – for example, the UK is allocated around 15% of Horizon 2020 funds which accounts for around 40% of this heading. Again, I have approximated the UK share of commitments by the payments data for the years 2014-2016 converted to 2020 prices. The result of these calculations is Column 3, which shows the commitment appropriations for the last year of the current MFF for the EU-27.

I assume that the Commission maintains the same level of expenditure on the other MFF headings even after the UK departure.

As noted above, I use the year 2024 as the reference year for the next MFF period. As a starting point, I assume that, apart from CAP direct payments, all other expenditure will be held constant in real terms. This gives me an initial estimate for the commitments budget in 2024. However, under Oettinger’s approach we have to find €9 billion in savings which I assume will be found solely in Headings 1 and 2.

The impact of inflation on the real value of direct payments automatically reduces Heading 2a by 8% and a reduction of 7% in the other headings (1a, 1b and 2b) would be sufficient to produce the necessary savings (note that Heading 1a is actually only reduced by 3.5% because around half of the 2020 expenditure under this heading is allocated to Horizon 2020 and ERASMUS+ which will be exempt from cuts).

Finally, to complete the MFF for 2024 we need to add in the proposed €12.5 billion expenditure on new priorities. This gives a total MFF (on an annual basis) in 2021-2027 of €164.9 billion in 2020 prices, compared to MFF commitments for the EU-27 of €161.5 billion in 2020, the last year of the current MFF.

Note that, on the basis of these assumptions, the share of cohesion (Heading 1b) falls to 32% while CAP spending falls to 30% of total MFF commitments in 2024 (the share for Heading 2 in total falls to 32% but this also includes spending on fisheries policies and the LIFE environment and climate programme).

A slightly larger cut than 7% in cohesion funding to bring it down to 30% of the total would free up sufficient resources to avoid any cut in CAP rural development spending. While one can easily imagine other permutations of the numbers, my conclusion is that, given Oettinger’s spending parameters, no significant cut in CAP spending over and above the impact of inflation on direct payments will be required in the next MFF.

Increased Member State contributions

However, Oettinger’s proposal also has implications for the gross contributions of the EU-27 Member States, and already Member States are queuing up to say they should not have to pay more into the EU budget because of Brexit (for examples, see the Dutch view here, the Swedish view here, the Austrian view here, whereas the German view appears to be more accommodating depending on how the additional funding is spent).

What is not entirely clear from these protestations is whether these countries are casting their bottom lines in terms of absolute amounts or shares of GNI. The implied increase in gross contributions from Member States in Oettinger’s proposal is €16.5 billion (€6.5 billion to cover half of the Brexit bill and €10 billion to cover 80% of spending on new priorities). In a total MFF budget of around €160 billion, this is an increase of around 10% in gross contributions on average.

However, as I discussed in this post, the burden of extra contributions does not fall equally on Member States because of the operation of the ‘rebate on the UK rebate’. If this is also abolished, then four Member States – Austria, Germany, Netherlands and Sweden – will be asked to pay disproportionately more, possibly up to 15% more. Whether this is politically likely or not will only become clear as the negotiations progress.

The other way of looking at gross contributions is as a share of EU GNI. In previous MFF negotiations, net contributors in particular had insisted that the EU budget should not exceed 1% of EU GNI in commitment appropriations (originally payment appropriations). Recall that Commissioner Oettinger is proposing that this should be raised to somewhere between 1.1% and 1.2% of EU-27 GNI.

Here, my speculative budget looks more reassuring, although the margin of error in the assumptions that I make is also greater. I have derived the EU-28 and EU-27 GNI in 2020 by taking the 2018 EU-28 GNI by Member State used to calculate the own resources shares in the 2018 EU budget and grossing up by 3.8% per annum (assuming 1.8% real growth per annum and the 2% MFF inflation factor). I have used the same formula to project EU-27 GNI forward to 2024 (but this time only using the 1.8% real growth factor as the 2024 figures are denominated in 2020 prices).

There are three observations to be made on the resulting figures:

• The 2020 figures show that the EU-28 commitment appropriations in the final year of the current MFF will be just under 1% of EU-28 GNI.

• Note that on the EU-27 budget on a ‘business as usual’ scenario in 2020 would be considerably higher, at 1.13%. This is the result of Brexit, and the exit of a Member State which makes a larger contribution to EU revenues than it receives in EU expenditure.

• Commissioner Oettinger’s proposal is for a relatively modest increase in overall EU MFF expenditure commitments of €3.5 billion. This would bring the EU budget share to 1.15% of EU-27 GNI. However, this fails to take into account the growth in EU-27 GNI over the MFF period. Assuming growth of 1.8% per annum means that in 2024 (the average year in the next MFF period), the budget share would have fallen back to 1.07%. This figure is a little smaller than Commissioner Oettinger’s request for an MFF of 1.1x% of EU-27 GNI.

Conclusions

Readers should not put too much weight on my speculative MFF budget, although I would welcome feedback if anyone feels that I have left out some important consideration.

The bottom line is that the Commission’s MFF proposal is likely by and large to shield the CAP budget from further unexpected cuts. However, it will also require additional gross contributions from Member States, substantial in some cases, as well as a small increase in the share of the EU budget in EU-27 GNI.

The MFF negotiations will not be easy, they never are.

This post was written by Alan Matthews

Photo credit: Wikipedia, under a Creative Commons licence